Welcome to the last part of my AIM journey.

After 38 parts, we take a look at the last 25 tickers today. The grand final is not a great final, there have been many many better parts. Three for my watchlist, most interesting is a well managed brewery/pub/bedrooms business.

Next week, expect a wrap-up of this whole series with some reflections on doing an A-Z for the first time, how I did it, what I would do different, …

Afterwards, I will continue with an A-Z on the Main Market and keep an eye on the AIM market with more or less regular AIM updates.

Thanks to everyone who followed along, read, liked, shared, commented, sent a DM or hated me for not anticipating a mining shitco pump.

Let’s go to AIM, one last time.

Here you find the last part:

Here you find all other parts: https://increasingodds.substack.com/s/a-z-uk-aim

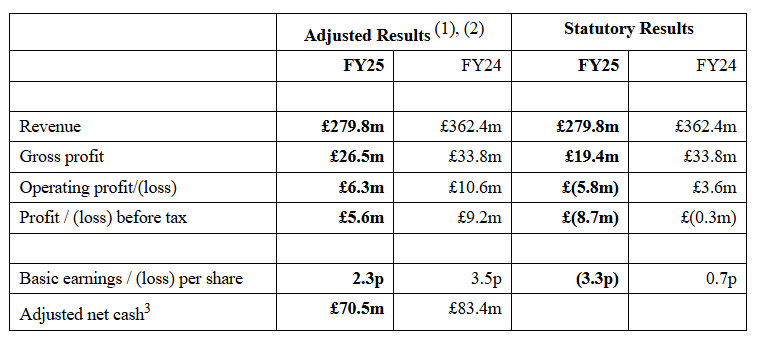

623) Watkin Jones (Ticker: WJG)

75£m residential for rent developer and operator. Latest results show a slowdown, but revenue includes sales of developments which are bumpy by nature:

Statutory results include a bigger impairmant and a 5£m safety provision. Reports pipeline of over 2£b, ROCE of 11,6%. 124£m NAV, 3,5% dividend, some smaller buybacks in recent years. Also operates in the student accomendations market. Considers itself to be well positioned to benefit from limited supply but increasing demand. Pass.

624) Wellnex Life (Ticker: WNX)

7£m unprofitable ‘brand and distribution company focused on the consumer health & wellness industry’, selling sleep aid, vitamin capsules, teeth whitening and pain relief products. Turnaround and restructuring ongoing, with ‘decision to consolidate and deprioritise non-core assets’ → ‘The Company has received unsolicited preliminary interest from separate parties regarding the acquisition of Pain Away (one of their brands) and other assets. Early-stage due diligence is underway across both approaches.’ Non-current assets only consist of intangibles, current liabilities > current assets, 2,5£m long term debt. Cash burn has been reduced but is still negative in H1, but Q2 was breakeven, 6£m H1 revenue. Pass.

625) Westminster Group (Ticker: WSG)

4£m unprofitable ‘supplier of managed services and technology-based security solutions’. Suspended due to delayed annual report. Announced 2£m in new contracts and created a new defense division. Raised 1,2£m. Apparently focused on airport security. Wants to expand in the Middle East, got multiple contracts with African airports. Not talking about profitability. Pass.

626) Westmount Energy (Ticker: WTE)

5£m O&G investment company with investments in the Guyana-Suriname Basin (South America). Got licenses in Falkland Islands. Pass.

627) Windar Photonics (Ticker: WPHO)

32£m provider of ‘LiDAR-assisted monitoring and optimisation solutions’ for wind turbines to monitor turbine generators or gather wind data. Operates unprofitable since ever, but now at least expects to be EBITDA neutral for FY25. Highlights delayed projects in China: ‘Company remains sensitive to large single orders’. Only number that is consistently growing is shares outstanding. Debt free, wants to grow in FY26, but far from profitable. Pass.

628) Winking Studios (Ticker: WKS)

58£m video game development and art studio from Singapore, the 4th largest globally. FY25 revenue mainly driven by M&A:

1/3 of revenue from China. Talks about maintained gross margin, ignores lower profit margins which descreased because the headcount increased by 70%. Wants to ‘establish operational presence in Western markets’. 20£m net cash, small dividend, no buybacks. 1/3 of revenue from follow-up projects. The recent acquisition adds a higher share of AAA console games. Founder-led. Pass.

629) Winvia Entertainment (Ticker: WVIA)

Recent IPO. 236£m provider of ‘price drawing and online gaming technology’. Describe themselve as a 'roll up in the UK price draw market’. It seems their model works like this: They set up a competition for a car valued at 50£k, customers can buy tickets to enter the competition. If they sell tickets for more than 50£k, that’s their profit. Which is just unfair gambling. Customers can pay monthly for tickets. Their ‘online gaming’ segment reflects online casinos in Romania, of course. FY25 adj. EBITDA of 31£m. Pass.

630) Wishbone Gold (Ticker: WSBN)

19£m no-revenue gold exploration company with projects in Australia. Pass.

631) Wynnstay Group (Ticker: WYN)

90£m supplier of agricultural products and services. FY25 results looking good, at least when excluding costs related to ‘Group-wide operating asset review and integration activity to establish a more efficient operating model’:

Improved pricing and products mix, revenue down due to subdued feed markets. Is focused on increasing adj. operating profit margin to 2%, wants to grow 10% a year by doubling the share-of-wallet of customers, adj. EPS is supposed to grow by 20% a year. New management since 23/24. 4,5% dividend, 132£m NAV. Best of the business is the own store segment, while the fertiliser and feed production segments produce <10% ROA. It’s a tough market to operate in, they will always be exposed to price fluctuations and thin profit margins, rather a pass, but seems like a solid business given the circumstances.

632) Wynnstay Properties (Ticker: WSP)

24£m commercial property company, with 18, rather small, industrial properties in the UK. H1 results looking okayish:

Lower profits due to costs for refurbishments, revenue growth from higher rents. 3% dividend. 8 leases expiring in H2, negotiations ongoing. 31£m NAV, properties valued at 46£m. NAV per share grew by 30% over 5 years. Chair owns 32%. Doesn’t look bad, but also nothing sparking my interest here. Pass.

633) Xeros Technology Group (Ticker: XSG)

11£m ’creator of technologies that reduce the impact of clothing on the planet’ used in washing machines. Barely any revenue, but highlights a ‘breakthrough Launch Agreement with one of the world's largest, branded washing machine manufacturers’ → ‘The intended outcome of the Launch Agreement is the mass production of domestic washing machines using Xeros' laundry care technology’. Three other customers are in ‘technical verification’ processes. Received an order from MediaMarkt for their in-house brands, one of the largest and best known consumer electronics retailers in Germany (parent company was sold to JD.com for 2€b). Obviously Xeros is early stage, but seems to gain some traction. No founders involved, no insider ownership. Pass.

634) XP Factory (Ticker: XPF)

19£m operator of escape-rooms and ‘Boom Battle Bars’, which ‘combine competitive socialising activities with themed cocktails, drinks and street food in a high energy, fun setting. Activities include a range of games such as augmented reality darts, Bavarian axe throwing, ‘crazier golf’, shuffleboard and others.’ Just lowered expectations to adj. EBITDA of 5£m to 6£m due to weak performance of Boom Battle Bars and higher labour costs. Board will ‘moderate’ the pace of new site openings and considers FY27 to be a year of ‘consolidation’. New Chairman is the CEO of TRU (Number 596 of this series), CFO will step down. XPF generally operates unprofitable and operating cash flow is completely used for growth capex and lease payments, so the current tough times may be a good trigger to head towards profitability. Not my cup of tea, pass.

635) Xtract Resources (Ticker: XTR)

13£m no-revenue exploration and development company focused on copper and gold with projects in Australia and Zambia. Share price just doubled. Pass.

636) Yellow Cake (Ticker: YCA)

1,55£b group holding uranium. ‘Yellow Cake seek to generate returns for shareholders through the appreciation of the value of its holding of U3O8 and its other uranium-related activities in a rising uranium price environment. The business is differentiated from its peers by its ten-year Framework Agreement for the supply of U3O8 with Kazatomprom, the world's largest uranium producer.’ Uranium holdings worth ~1,3£b. Shares out trippled in the last 5 years. Pass.

637) YouGov (Ticker: YOU)

219£m research data and analytics group, some may know the name from political surveys. New Chair. Trading update reports low-single-digit revenue growth, cautious customer spending and ‘operating profit delivery will be dependent on cost management’, sounds like margin pressure. Adj. operating profit of 60£m last year (45£m when excl. reorganisation costs and other bla bla). About 20£m FCF a year (incl. growth capex), 5% dividend, 140£m net debt. Paid 260£m for an acquisition in H1 2024, now rebranded as YouGov Shopper where participants can scan purchases to earn vouchers. Some AI talk how its integrated in their data analytics. YouGov has the advantage of collecting the data AI can use, so I don’t see it as a threat. Detailed write-up by @Alex Sweet from 2024:

Co-Founder returned as CEO in 2024, but his position is only considered to be ‘transitional’. Board expects him to stay for FY26. There are no medium-term financial goals as far as I can tell, the strategy part in the recent presentation is rather corporate bla bla. I’d say it’s cheap enough to keep an eye on. Watchlist.

638 & 639) Young & CO’s Brewery (Ticker: YNGA & YNGN)

460£m operator of pubs and bedrooms. Wants to list on the Main Market. Operational performance over the Christmas season was ‘very strong’, with 11% revenue growth. 10£m buyback ongoing. H1 results ending Sep 25 looked good as well:

Performance simply driven by ‘good momentum’. Worth noting that increases in minimum wage were completely passed apparently. Usually businesses like this cry about cost inflation. 3% dividend and paying down debt, about 50£m FCF a year, NAV of 800£m. Mostly owns their locations, not many leases. CEO joined in 2022, worked for Pubs and Breweries his whole life. A directors owns 11%. Was heavily hit by Covid of course, but except that, revenue is growing year by year with stable margins. This seems to be one of the rare leisure businesses I’m interested in. 11x fwd. P/E (Koyfin). Watchlist.

640) Yü Group (Ticker: YU.)

283£m ‘supplier of gas, electricity, meter asset owner and installer of smart meters.’ TU highlights 48% growth in ‘supplied meter points’, what refers to the numbers you find on electricity and gas meters at home I assume. FY25 revenues of 700£m and EBITDA of 50£m (PBT ~10% less than that). Management is confident to ‘perform against all key performance indicators in FY26.’ 2,7% market share. Talks about investments in headcount for smart meters, but reduced engineering headcount by 30%? 3,5% dividend, debt free. Profitability consistenly growing since 2018. CEO and Founder owns 52%, COO just joined from a water supplier. The smart meter market is highly competitive, with 10+ bigger players fighting for market share. Got a hedging agreement with Shell. I don’t really have an idea how these energy supply markets work and look like, but Yü’s financials look too interesting to ignore it at this valuation. Watchlist.

Overview by @The Value Bandit:

641) Zambeef Products (Ticker: ZAM)

14£m ‘cold chain food products and retail business with operations in Zambia, Nigeria and Ghana.’ Trades at 2x last years profits, at least on a first glance, but all cash flow is eaten up by capex. NAV of 200£m. But apparently I am missing something here, I only found this write-up from 2024, stating that the EV is more than 10x the market cap, but I am not sure why that’s the case. UK government owns 17,5%. Pass.

642) Zanaga Iron Ore Company (Ticker: ZIOC)

50£m no-revenue mining company with an iron ore project. Raised 23$m, mainly used to repurchase an equity stake from Glencore for 15$m. Reports 5,2$B net present value of project and a 27% project IRR. Pass.

643) Zenova Group (Ticker: ZED)

Suspended ‘fire safety and heat management solutions company’, due to a potential acquisition. No details disclosed, more information expected mid-May. Operates highly unprofitable with low revenues. Pass.

644) Zephyr Energy (Ticker: ZPHR)

75£m highly unprofitable O&G company with projects in the US. Announced a partnership to fund investments up to 100£m. Pass.

645) Zinc Media Group (Ticker: ZIN)

10£m content creation company of shows, movies and documentaries. FY trading update shows 27% growth in revenue and adj. EBITDA to 1,9£m. 21£m pipeline. Reports a good start to FY26. Medium term target of 50£m revenue and 5£m adj. EBITDA. Still prints an unadjusted loss, but is operating cash flow positive. CEO got a media background. Not my cup of tea, but it seems ZIN is on a good path to consistent profitability in a competitive industry. Pass.

646) Zinnwald Lithium (Ticker: ZNWD)

37£m no-revenue lithium company owning the Zinnwald Project in Germany. Reports ‘strong support’ from german federal government and completion of some planning procedures required for further planning. As a German I can tell you, these procedures take forever, we love bureaucracy. Pass.

647) Zoo Digital Group (Ticker: ZOO)

13£m unprofitable ‘provider of services allowing TV and movie content to be subtitled and dubbed in any language and prepared for sale with all major online retailers.’ Just won two customers. Cost savings implemented and says underlying operations are cash generative now. Revenue down 20% YoY, but sees a bottom, benefitting from FY24 Hollywood strikes which led to an increased backlog. Is actively integrating AI into workflows, e.g. subtitling delivered in 3 hours instead of 1-2 weeks. While this is great from an efficiency perspective, it raises the question why customers should rely on ZOO when it becomes that easy to subtitle. Apparently works with thousand of freelancers. Trading in line with market and board expectations, no idea how they look like. Pass.

Wrap-up

646/646 companies covered in total (a couple more tickers due to unique share structures)

Watchlist: 98/646.

Pass: 548/646.

No-Revenue counter: 129/646.

Feel free to provide opinions and sources on any of the stocks. Cheers.

Watchlist

Part 1: 4GBL (Delisted), ABDP, ASCO, AMS; Part 2: ALT, ALU, AMCO, ANG; Part 3: ANCR, AT, AVG, BPM; Part 4: BGO, BEG, BIG, BRCK; Part 5: CBOX; Part 6: CLBS, CEPS, CER, CKT, CHH Part 7: CFX; Part 8: CSSG, CRPR, CVSG; Part 9: DFCH, DOTD; Part 10: EAAS; Part 11: None; Part 12: FIN, FNTL, FKE; Part 13: FLO, TUNE, FRAN, GBG; Part 14: DATA; Part 15: HDD, HAYD, HERC; Part 16: IDOX, ING; Part 17: JNEO, JDG; Part 18: KITW; Part 19: LST, WINK; Part 20: MLVN, MBH; Part 21: MAB1, MWE; Part 22: WINE, NWT, NTBR; Part 23: OHGR, OGN; Part 24: OMG, PEB; Part 25: TPFG; Part 26: QTX, REAT, RLE; Part 27: RCN, RNWH, RGG; Part 28: ROSE, RTC, RWS, SDG; Part 29: SAG, SDI; Part 30: SRC, SFT; Part 31: SAL, SPSC/SPSY, SRT, STAF, KETL; Part 32: SUP; Part 33: TAM, TIG; Part 34: TMG, PEBB, WRKS; Part 35: TFW; Part 36: TRT, TRU; Part 37: UPR; Part 38: VNET, VLX, VLE, VUL, WATR; Part 39: YOU, YNGA/YNGN, YU.

Just a couple of comments. A year or two after WJG was floated the founding family members sold all their shares in the business and headed for the hills. That was more than an omen! YNGA is a well-respected business, with a great product. the asset backing may seem stronger than it really is though. A pub worth say £1m, if it becomes redundant, turns into a building worth a quarter of that. This example may also be further complicated by the fact several of their premises are listed, and conversion to alternative uses may be awkward. Having said that, I think you are bang on: this is certainly a business worth watching.

Finally, can I just say "thank you" for all your hard work, intelligence and diligence here. I have found your work really informative, entertaining and useful. I am truly grateful for your willingness to share here.