AIM A-Z Part 36: Potential Exit, Buybacks, Adjustments

Ticker 586 to 600 on London's Alternative Investment Market (AIM)

Welcome,

reaching ticker 600. There are 47 tickers left to look at after this part (more than I thought last time, did a mistake when looking at my list). So expect 3-4 more parts. I will continue with the Monday & Friday schedule until we reach the last ticker.

Two for the watchlist today, most interesting is a company, where a new share structure in a subsidiary suggests a potential sale. Let’s go.

Here you find the last part:

Here you find all other parts: https://increasingodds.substack.com/s/a-z-uk-aim

586) Touchstone Exploration Inc (Ticker: TXP)

27£m unprofitable O&G company with projects in the Republic of Trinidad and Tobago. Also listed in Canada. Pass.

587) Tower Resources (Ticker: TRP)

8£m no-revenue O&G company with projects in Africa. CEO owns 21%. Raised cash three times in the last 4 months. Pass.

588) TPXimpact Holdings (Ticker: TPX)

41£m IT consulting company focused on digital transformation. Share price just doubled due to large contract announcements: ‘DEFRA (£39m), NHS England (£22m with an option to extend to £33m) and an uplift to the existing £49m contract with HMLR (£11m).’ Focus on public sector. Expects at least 7£m adj. EBITDA for FY26 and will reveal a three-year plan soon after successfully executing on its plan to reduce debt and increase (adjusted) margins in the last three years after the current CEO joined, who previously led EY’s public sector team.

Reports an operating loss mostly due to the amortization of acquired intangibles and restructuring costs. I randomly picked an older annual report and these restructuring costs already occurred in 2021 and 2020 … and probably in every other year too. Ignoring SBC and restructuring, adj. EBITDA can be cut in half. Very likely some customer/contract concentration. 12x EV/my adj. EBITDA. Pass.

589) Tracsis (Ticker: TRCS)

106£m ‘provider of software and hardware products, data capture and data analytics/GIS services for the rail, traffic data and wider transport industries.’ H1 trading update highlights contract wins, expect at least 13£m adj. EBITDA for the full year, net cash of 25£m. Includes over 2£m costs related to ‘the transformation of the Group's operating model’, meaning restructuring of divisions, SaaS rollout, … at least I didn’t find restructuring costs in an old annual report here. But some work is needed to figure out what this transition really is. 30% recurring revenue, completed a 3£m buyback. Reported FCF of 7,7£m last year. Focus is on M&A of growing the recurring revenue. New CEO since August, engineering background. Interesting niche, but I struggle to see the elevator pitch here. Pass.

590) Trafalgar Property Group (Ticker: TRAF)

0,4£m ‘residential homes and assisted care development business’. Revenue reflects sale of developed sites. Sold a site for 0,7£m, but still reported an operating loss and invested some of the cash inflow into a 10% stake in an office building, apparently that’s their only project right now. Pass.

591) Transense Technologies (Ticker: TRT)

10£m ‘developer of specialist wireless sensor systems used to enable real-time data gathering and monitoring’. Stock price just got cut in half after a trading update suggested weak H1 results, with decreased revenue and roughly break even performance. Most of revenue is related to a 10-year licensing deal with Bridgestone ending in 2030 and part of that deal was a reduction in received royalty from 1 July 2025, explaining some of the decrease in revenue. This deal was also the reason for TRT to turn profitable. I watch TRT on my watchlist since the article below, but never took a closer look. It’s a small niche business with the obvious headwind of a major contract expiring soon. The article is from 2023, but is really detailed, by @mavix:

592) Trellus Health (Ticker: TRLS)

2£m provider of a ‘digital platform that integrates data analytics with personalised, scientifically proven resilience programmes and value-based solutions to manage complex chronic conditions’. Announced a 6 month contract extension with Johnson & Johnson, got licensing agreements with Pfizer and AstraZeneca. Received a loan from a shareholder. 0,4£m revenue on adj. EBITDA loss of 2,6£m. Pass.

593) Tribal Group (Ticker: TRB)

150£m provider of education software and services. Meaning student information systems to manage exams, onboarding or file management. Expects 91£m revenue and 16,5£m adj. EBITDA for FY25, net cash. 63£m ARR, SaaS transition is ongoing. A competitor from Ireland acquired 26% of shares in 2023 to block a takeover bid from Ellucian, another competitor. Paid down its debt and recurring revenue is becoming more and more important. Wants to grow by upselling and winning more customers. Adj. EBITDA is adjusted for amortization of capitalized development costs and again for restructuring. Ignoring that leaves you with 7£m adj. EBITDA for H1 instead of 8,3£m. Pass.

594) Tristel (Ticker: TSTL)

196£m infection prevention company focused on decontamination of medical device and surface disinfection. H1 trading update highlights 14% revenue growth with increased adj. EBITDA margin to 28% and good performance in the US. CEO will leave, he just joined in late 2024 and replaced the founder. Growth driven by international expansion, entered Spain, India and Austria last year. The US market is a main focus. Wants to ‘sustain double-digit revenue growth’. Seems like a quality company looking at its financials, 3,5% dividend, consistent revenue growth and stable margin. 23x fwd. P/E (Koyfin). Multiple management changes, some share dilution and customer concentration (27% of revenue from one customer) raise doubts about the quality label though. Pass.

595) Truetide (Ticker: TRUE)

2£m investment company with a focus on early stage biotech and technology companies. NAV of 2,7£m. CEO owns 27%. Pass.

596) Trufin (Ticker: TRU)

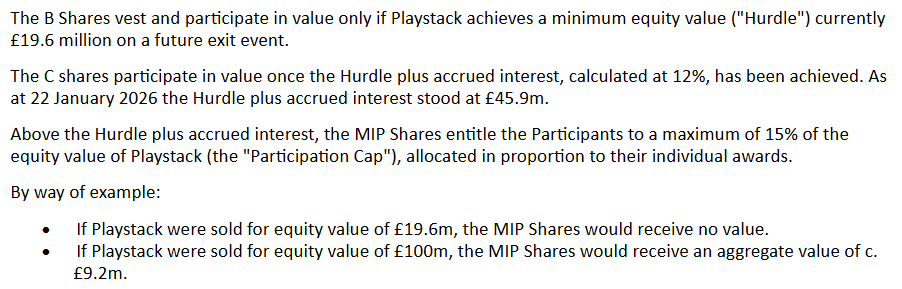

116£m group owning three companies: a ‘provider of Early Payment Programmes and a specialist in payments control and market insights’, a fintech focused on working capital solutions for SMEs and a video game publisher focused on indie games. Interestingly, the CEO of the video game publisher has been awarded with new shares, allowing him to receive payments in case of a sale:

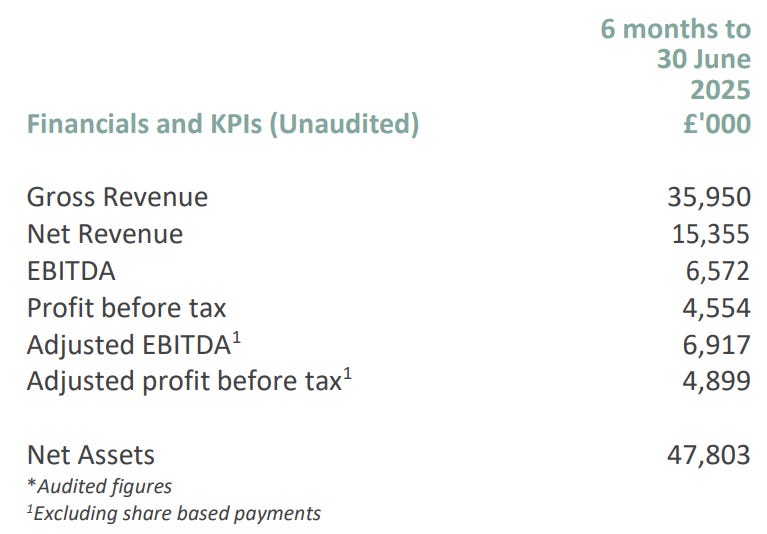

TRU is debt free, two founders are CEO and CFO. Biggest shareholder is a PE company and TRU is a spin off from another investment company. Recent results looking good:

Results mainly driven by good performance of the video game publisher (~5£m EBITDA). Nevertheless, financials are rather bumpy. Repurchased 10% of shares last year, just announed a new 6£m program. 15x fwd. P/E (Koyfin). There have been two smaller exits in 2023 and 2024. I’d say it’s worth to keep an eye on TRU, watchlist. Write up:

597) Tungsten West (Ticker: TUN)

349£m producer of tungsten and tin owning the world’s third largest tungsten resource. Share price trippled in January after Henry Maxey doubled its shareholding to 14% (no idea who that is, but got the same last name as a director) and another investor acquired a 30% stake. Surprise, two weeks later TUN announced that the net present value of their project increased 10x to 1,7$b and the IRR increased from 27% to 197% driven by trippled tungsten prices, apparently due to stricter export controls in China. After the share price’s jump, TUN raised 30£m. Pass for me, but might be worth a look for others. Write up:

598) UK Oil & Gas (Ticker: UKOG)

6£m unprofitable company developing a hydrogen storage site in the UK. Makes some little revenue with an oil field. Shut down operations in Turkey. Pass.

599) Ukrproduct Group (Ticker: UKR)

3£m producer of dairy products and kvass (fermented bread drink) with production plants in western Ukraine. Latest results looking solid, except the currency losses.

Revenue growth mainly driven by exports and inflation. Generally highlights the obvious challenging environment to operate production sites in a war. Describes liquidity as ‘constrained’. Trading update from December describes increased electricity outages and limited availability of workforce and raw products and higher costs. Profit margin is ‘under pressure’. Pass.

600) Ultimate Products (Ticker: ULTP)

46£m owner of various brands for houseware. Moved from Main Market to AIM. H1 results show -6% revenue due to continued weak customer sentiment with 5£m adj. EBITDA. Expects 10£m for the full year, should be around 5£m in profits → 9x P/E, pays 50% of profits as dividend. President & Founder owns 21%. The product portfolio seems to be fairly basic spanning every aspect of houseware you can imagine, distributed through retailers like Tesco and Lidl, but also online. 2/3 of sales in the UK. I’d say it’s overall a solid business, but the case really depends on consumer sentiment to get better. Further it’s a competitive field to operate in. Not a big fan, but valuation leaves room for upside in case of sentiment upticks. Pass. Good write-up by @Adrian Ford :

Wrap-up

600/669 companies covered so far.

Watchlist: 89/600.

Pass: 511/600.

No-Revenue counter: 121/600.

Feel free to provide opinions and sources on any of the stocks. Cheers.

Watchlist

Part 1: 4GBL (Delisted), ABDP, ASCO, AMS; Part 2: ALT, ALU, AMCO, ANG; Part 3: ANCR, AT, AVG, BPM; Part 4: BGO, BEG, BIG, BRCK; Part 5: CBOX; Part 6: CLBS, CEPS, CER, CKT, CHH Part 7: CFX; Part 8: CSSG, CRPR, CVSG; Part 9: DFCH, DOTD; Part 10: EAAS; Part 11: None; Part 12: FIN, FNTL, FKE; Part 13: FLO, TUNE, FRAN, GBG; Part 14: DATA; Part 15: HDD, HAYD, HERC; Part 16: IDOX, ING; Part 17: JNEO, JDG; Part 18: KITW; Part 19: LST, WINK; Part 20: MLVN, MBH; Part 21: MAB1, MWE; Part 22: WINE, NWT, NTBR; Part 23: OHGR, OGN; Part 24: OMG, PEB; Part 25: TPFG; Part 26: QTX, REAT, RLE; Part 27: RCN, RNWH, RGG; Part 28: ROSE, RTC, RWS, SDG; Part 29: SAG, SDI; Part 30: SRC, SFT; Part 31: SAL, SPSC/SPSY, SRT, STAF, KETL; Part 32: SUP; Part 33: TAM, TIG; Part 34: TMG, PEBB, WRKS; Part 35: TFW; Part 36: TRT, TRU

Made new write up on Trufin: https://miroslavstepanek.substack.com/p/trufin-trul-eng