AIM A-Z Part 38: 5x Watchlist, the best part?

Ticker 613 to 622 on London's Alternative Investment Market (AIM)

Welcome, 5 watchlist companies today. Only 10 tickers, but these were interesting enough. We also come across the only AIM company I own so far, Volex. Even the tickers I passed on might be interesting: we have a turnaround case, an online wine retailer with a big buyback program and UK’s leading bathroom retailer. I’d say this is the best part of the whole series.

Here you find the last part:

Here you find all other parts: https://increasingodds.substack.com/s/a-z-uk-aim

613) Vianet Group (Ticker: VNET)

20£m ‘provider of actionable data, business insights and payment solutions’, meaning payment, data analytics and inventory management service for hospitality and unattended retail (e.g. vending machines). Trading update highlights postponed investments of customers, nevertheless reports 10% H1 EBITDA growth to 1,9£m. Full year profits will be in line with last years (3,4£m EBITA) due to ‘slower rate of deployment, ongoing strategic investments in the Beverage Metrics platform, and the discontinued ERP platform income’.

27£m NAV, mostly intangibles, basically debt free, 84% recurring revenue, 2% dividend, small buyback last year. CEO/Chair owns 19% and is with VNET since over 20 years. Revenue suffered heavily from Covid, so either the ‘recurring’ revenue is transaction based or the subscription based model was mainly implemented afterwards. Growth case seems to be build around finding more customers. 6x EV/EBITA. Looks interesting, watchlist.

614) Victoria (Ticker: VCP)

27£m manufacturer and distributor of flooring products. Profitability (and the share price) are crashing since 2023. Reports an adj. loss before tax of 15£m for H1 alone, or a loss of 140£m without adjustments with 1£b net debt and negative equity, yes billion. Highlights weak consumer demand with demand 20-25% below the long-term trend. Adjustments mainly relate to relocation of production to Turkey and refinancing costs. Management is working on increasing margins by laying off employees and property disposals in Belgium. Liquidity seems at least constrained with about 100£m in capex, lease and interest expenses. Hired a new CEO labeled as ‘growth-oriented and turnaround CEO’. Latest trading update lowered adj. EBITDA expectations by about 15%. Might be one to watch for turnaround investors, but it seems too early to tell whether this works out. Pass.

615) Victorian Plumbing Group (Ticker: VIC)

263£m ‘UK's leading’ bathroom retailer. Founder who was CEO just stepped down, will remain on the board and will be replaced internally by a managing director who joined in 2013. Reported 9% growth at the AGM with maintained margins driven by volume. Latest FY results looking solid:

2024 numbers include costs from warehouse transformation and exceptional M&A costs. PBT down due to higher leasing expenses from a new distribution center. Debt free, 2% dividend. 81% of revenue from own brands, spend 27% of revenue on sales & marketing. Revived an online furniture brand (went bankrupt in 2008) which now generates first revenues for VIC. Founder and his brother own 57%. Wants to grow in the tiles & flooring market, currently holds about 1%. Three biggest competitors are B&Q and Wickes and Ikea. Seems solid overall, I just don’t see the elevator pitch. Tiles and flooring and the general furniture online shop are still too small to drive meaningful growth. Therefore, rather a pass. 16x fwd. P/E (Koyfin).

616) Virgin Wines UK (Ticker: VINO)

29£m online wine retailer. 15% buyback ongoing, 10£m net cash. Reports a return to growth over the christmas season with 5% growth, or 2% over whole H1 period. Similar to Naked Wines (Numer 393), customers have cash deposits they receive interests on and gives them access to exclusive deals. 60£m revenue on 1,6£m PBT. Wants to reach 100£m revenue and is confident to match undisclosed market expectations for 2026. CEO owns 9% and formed VINO through a merger with a company he founded. Revenue and wine club members flat since 3 years. Will launch its own app. Is focused on growing through partnerships, e.g. with Moonpig (greeting cards retailer). Not my cup of wine. Pass.

617) Volex (Ticker: VLX)

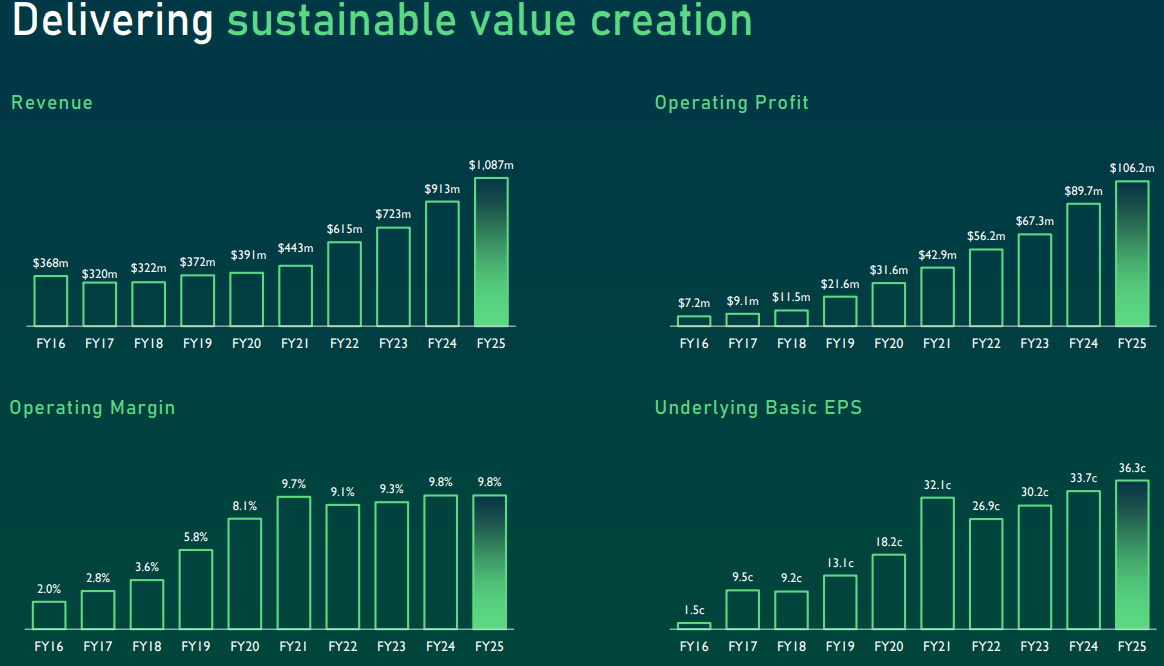

The first company in this series I already own, since 2024. 844£m manufacturer of power and data transmission products such as power cords, plugs, connectors, cuircit boards or data transfer cables needed for consumer electronics, EV charging or data centers. Looking at the long-term share price it was a wild ride. Current CEO took over in 2015 and successfully turned VLX around, he owns 25%. Latest results looked good:

Expanded multiple production sites, growth driven by EV, data centers and a one-off project in the off-highway segment. This segment was built up through a big acquisition in Turkey. Data centre revenue is about 6% of revenue. Demand from medical and consumer electronics remains subdued since the covid boom. Below you see the performance since the current CEO joined:

Performance driven by M&A and organic improvements. VLX both operates in high-volume, low-price markets but also in more specialized areas. Best known competitor is the industrial giant Amphenol. Will reach its FY27 targets of 1,2£b revenue with 9-10% adj. EBIT margins. About 10x fwd. EV/EBITA. Did not really suffer from tariffs. I bought VLX as it was trading at about 10x fwd. earnings. It’s not that cheap anymore, I consider it more or less fairly valued at the moment. The underlying markets tend to be cyclical, but VLX is well diversified.

It’s the first time I can link articles of myself. I wrote about VLX twice (I should do an update). While these articles are not up to date, I’d say they give a good overview:

618) Volvere (Ticker: VLE)

54£m holding company with a focus on ‘under-performing’ businesses that need growth capital. Currently only owns two companies in food manucaturing after selling other businesses pre-covid. Repurchased 60% of shares since 2010 with continious buybacks. Is lead by co-founder Nocholas Lander, who took over after the death of his brother in 2023. Latest results looking good with 7% revenue growth and H1 increased profits of 2,2£m, NAV of 44£m with 28£m in cash. Is considering to expand production capacity. Not much communication, but the reports are straight to the point without much bla bla and the website looks like it’s from 2012, which is a good sign. I knew VLE before, can’t trade it anyways, but it’s one of the rare share cannibals on AIM with a great long-term track record. Watchlist. Wirte-up by @Myles Kuah:

619) Vulcan Two Group (Ticker: VUL)

15£m no-revenue company ‘aiming to create the UK's leading regulated ePharmacy through buy-and-build’. Signed a lease for a distribution center and raised 40£m to acquire three ePharmacy companies. The resulting group will generate about 35£m revenue, ‘with a high proportion of recurring revenues’ and ~3£m in profits. CEO got a M&A background and built a similar group in the contact lense market. The group was sold to EssilorLuxottica. CFO was CFO at Boku (>500£ market cap) and the Paysafe Group (known for Skrill and Paysafe Cards). CEO and CFO own 22%. Seems like a good management for a 15£m AIM company. Of course a lot of execution risk here, but one to watch. Watchlist.

620) W.H. Ireland Group (Ticker: WHI)

10£m unprofitable wealth manager. Will merge with another AIM listed, unprofitable wealth manager (Ticker: Team). WHI shareholder will receive 0,195 TEAM shares. Board got support from major shareholders. Pass.

621) Warpaint London (Ticker: W7L)

190£m supplier of colour cosmetics with multiple owns brands. Announced a 1,4£m acquisition out of administration for a company with 15£m revenue. FY25 revenue flat due to M&A activities, otherwise -9%, with adj. EBITDA of 22£m. 4% dividend. Highlights tariff disruption and weak customer sentiment. I am absolutely no interested in beauty groups due to the trend nature and dependence on retailers, pass. But @InvestingWithWes Newsletter shared his view a couple months ago:

622) Water Intelligence (Ticker: WATR)

49£m ‘provider of precision, minimally-invasive leak detection and remediation solutions’. Is repurchasing franchises:

9 months trading update confirms the momentum. Is ‘increasingly confident about expectations for 2026’. Considers itself to be a well positioned, partly the only end-to-end solutions provider in their markets (I doubt that). 10x P/E, small buyback ongoing. CEO who joined in 2010 owns 25%. Looks interesting overall and is cheap, but it also seems there is a lot going on and the reports have a lot of ‘we are amazing’ talk. Watchlist. @The Oak Bloke does a good job covering WATR:

Wrap-up

622/669 companies covered so far.

Watchlist: 95/622.

Pass: 527/622.

No-Revenue counter: 125/622.

Feel free to provide opinions and sources on any of the stocks. Cheers.

Watchlist

Part 1: 4GBL (Delisted), ABDP, ASCO, AMS; Part 2: ALT, ALU, AMCO, ANG; Part 3: ANCR, AT, AVG, BPM; Part 4: BGO, BEG, BIG, BRCK; Part 5: CBOX; Part 6: CLBS, CEPS, CER, CKT, CHH Part 7: CFX; Part 8: CSSG, CRPR, CVSG; Part 9: DFCH, DOTD; Part 10: EAAS; Part 11: None; Part 12: FIN, FNTL, FKE; Part 13: FLO, TUNE, FRAN, GBG; Part 14: DATA; Part 15: HDD, HAYD, HERC; Part 16: IDOX, ING; Part 17: JNEO, JDG; Part 18: KITW; Part 19: LST, WINK; Part 20: MLVN, MBH; Part 21: MAB1, MWE; Part 22: WINE, NWT, NTBR; Part 23: OHGR, OGN; Part 24: OMG, PEB; Part 25: TPFG; Part 26: QTX, REAT, RLE; Part 27: RCN, RNWH, RGG; Part 28: ROSE, RTC, RWS, SDG; Part 29: SAG, SDI; Part 30: SRC, SFT; Part 31: SAL, SPSC/SPSY, SRT, STAF, KETL; Part 32: SUP; Part 33: TAM, TIG; Part 34: TMG, PEBB, WRKS; Part 35: TFW; Part 36: TRT, TRU; Part 37: UPR; Part 38: VNET, VLX, VLE, VUL, WATR

Thanks for including my write-up in your article