Before we start I want to say I do not see this as a ‘deep dive’ or a ‘fat pitch’. I simply want write down my basic idea for an investment. There are things I don’t cover, I’m not aware of or which I misunderstood.

Volex Plc ($VLX.L) is a global manufacturer of power and data transmission products such as power cords, plugs, connectors, cuircit boards or data transfer cables needed for consumer electronics, EV charging or data centers. CEO Nat Rothschild, who owns ~25% of the shares, took over in 2015 and transformed Volex from a struggling, declining business facing pricing pressure and customer concentration into a well-run, efficient, more diversified player.

This has been achieved by focusing on areas with less high-volume, low-cost competition such as EV and high-end power cords, streamlining operations by restructuring or shutting down factories and offices, onboarding new customers and accretive M&A deals.

Today Volex operates in 5 main areas:

EV (13% of revenue): charging cables and plugs, recently awarded by Tesla to manufacture NACS couplers (in simple words: the thing you plug into your EV to charge it )

Company announcement Consumer electricals (26%): variety of wiring, cords, plugs, power products for wide range of applications in PC’s, monitors, notebooks, washing machines, …

Medical (17%): more complex cable assemblies, printed curcuit boards (PCB) and box builds for medical devices

Complex industrial technology (20%): Unique products for data centers, defense, robotics, telecom, …

Off-Highway (24%): PCB, custom wiring and cable harnesses for off-highways machines/vehicles like tractors, trams, excavators or fork trucks

The off-highway segment is now separately reported since the large acquisition of Murat Ticaret in H1 FY24 (more on that later).

It should be said that these markets are overall really competitive. Especially in mature consumer electronics markets we have low-cost producers in China but also big industrial giants like Amphenol. The competitive environment was one of the main issues prior to Nat Rothschild’s time and the environment didn’t change. But nowadays Volex got a way more competitve cost structure to compete in these areas if neccessary and on the other side is more focused on more specialised, higher margin, less competitive end markets. For example they will not compete in the european PCB market, as this is way more competitive than in the US, which is characterized by more local, specialized players

Numbers

Below I want to provide some overall numbers. Note that Volex is reporting in $, so all the numbers I provide are in $. Despite the turnaround and great development, Volex is not trading on super elevated valuation, but forward number that you’ll see further down are more relevant.

Part of the story is that we saw 3 share issues in 10 years. To shed some light:

2014: Equity raised by the old CEO to pay down debt

2018: Proceeds used for M&A and working capital

2023: Proceeds used for the Murat Ticacret acquisition

SBC ~0,5%-1% of market cap p.a.

Looking forward

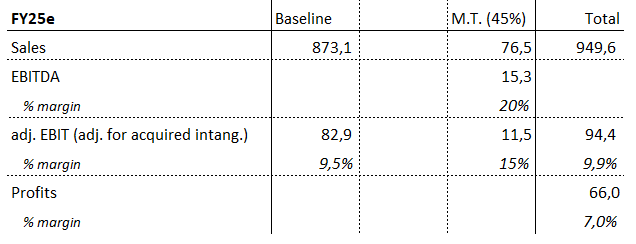

But it’s getting more interesting if we look forward. In H1 24 Volex acquired Murat Ticaret (M.T.) for a total consideration of up to ~$190m. Murat Ticaret will ad ~$170m in sales, with a 20% EBITDA margin which is way above the group level of ~11%.

The acquisition has been completed in September 2023. Volex fiscal year ends in April, so we can expect M.T. will contribute 55% of its sales and profits (assuming 20% EBITDA, 15% EBIT, expecting no seasonality) to the group for FY24.

To provide FY24 expectations I took the FY23 sales as a baseline. We already got H1 24 numbers that showed 4,2% organic growth, 11,2% total growth and margin increases. I expect 3% organic growth for FY24. ~$9,7m will be contributed from a FY23 acquisition with a 13% EBIT margin. I assume no organic growth in these acquired business here.

Based on these assumptions, we have a FY24e EV/adj. EBIT multiple of ~10.

Taking this further to FY25 to reflect the full contribution of M.T.: I again assume 3% organic growth from FY24e sales and the 9,5% adj. EBIT margin and just add the missing M.T. contribution:

Based on these assumptions, we have a FY25e EV/adj. EBIT multiple of ~8,6. I further assumed the profit margin to hit 7%, rougly increasing in line with EBIT margin, bringing Volex on a FY25e p/e of 10. Remember that Volex’s FY ends in April, so the FY25 numbers are the ones we see in a trading update in April 2025.

In terms of FCF I would expect to see margins between 6-7% going forward incl. growth capex. FCF is fluctuating a lot based on customer demand and customers inventory levels, basically ranging from negative margins to 10+% e.g. while covid due to destocking. But on average we see FCF slightly below reported profits. Capex in the last 2 years was ~2,5% of sales incl. growth capex.

These numbers ignore any further M&A deals or organic margin increases. The 3% organic growth estimate seems fairly conservative as Volex just doubled their prodcution space in Poland in H1 24, is expanding their factory in Mexiko and is building new factories in India and Indonesia, both are expected to go live in H2 FY24 or FY25.

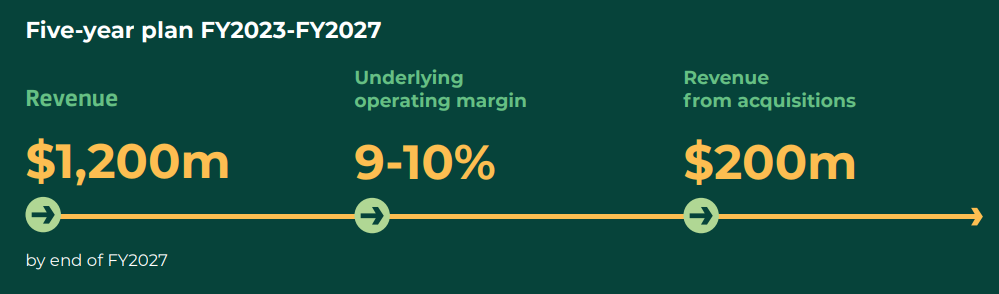

2027 targets

The *underlying operating margin* is basically an adj. EBIT margin for sbc, amortisation of acquired and intangibles and acquisition costs. I don’t agree on adjusting for sbc and acquisition costs as sbc is a real expense and acquistion costs are not one-offs if M&A is part of the strategy, so my numbers above are not the same as the company provides, but even my adj. EBIT, which is more conversative, hits the 10% margin in FY25.

The M.T. acquisition and the one in FY23 already bring us to $185m acquired sales, so the target is basically achieved. Considering that we have seen 2 M&A deals a year in the last 5 years, we will likely see >$200m acquired sales until FY27.

Also the sales target seems achievable. My estimates above are below broker expectations, but expecting further M&A deals and mid single digit organic growth would make us hit the target.

Especially because of the M.T. acquisition I would assume that the margin target will be updated to something like ‘10%+’.

Expected IRR

Volex is paying ~1% in dividends, but as mentioned is also diluting via sbc. So to keep it simple I would assume that sbc offsets the dividend return.

Keeping it straightforward, expecting $1.200m in sales with my more conservative adjusted 10% EBIT margin would give us $120m in adj. EBIT or a <7x EV/adj. EBIT. Using the 7% profit margin here would give us $84m in profits in 2027 or a <8 p/e.

As a reminder: the current fwd. EV/adj. EBIT is ~10.

10x $120m = $1,2B enterprise value at the end of FY27 (April 2027).

This implies a 47% increase from current levels in a little more than 3 years, or ~12% irr calculating with 3,25 years.

Risks

One customer in EV accounted for 15,8% of sales in FY23. Because of the M.T. acquisition the customer concentration should be decreasing here, but nevertheless remains a potential threat.

Large M&A deals always have the risk of not delivering what’s promised, so it’s important to keep an eye on the M.T. integration, cross selling, …

Further dilution, especially higher sbc levels or equity raises where the cash gets more or less burned would be a red flag.

Pricing pressure in some markets. I don’t see this as a big risk going forward as Volex becomes more specialized, but e.g. in FY23 we saw a -3% sales decline in consumer electronics despite a low single digit volume increase due to price deflation.

Wrap up

Overall I believe Volex is an interesting opportunity in an overall competitive market, in which it’s able to take the fight due to financial discipline and where Volex has found its niches. Nat Rothschild is well alligned due to its 25% stake and build his track record with financial excellence over the last 9 years.

I hope I could arouse some interest for Volex and my work might serve as a starting point for further research and discussions. Feedback is always welcome. Cheers.

Good article, they seem to have a similar profile as Hammond Power Solution - HPS.A TO.