Part 3: Navigating Growth Opportunities through Capital Allocation

Part 3: Navigating Growth Opportunities through Capital Allocation

The Investment Checklist: The Art of In-Depth Research

This is the third and last part of my wrap up of Michael Shearn’s book The Investment Checklist. In part 1 and 2 we mostly looked backwards.

Now it’s time to evaluate the future.

Capital allocation (Chapter 8 & 11)

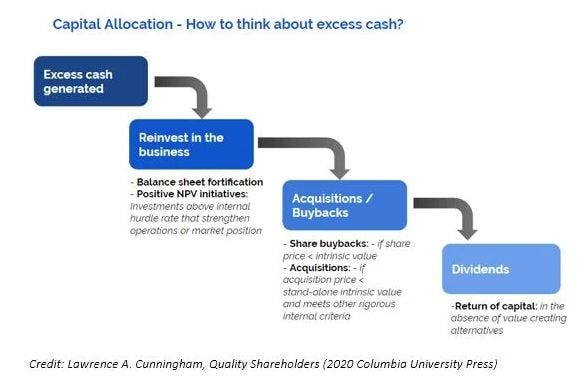

One of the main jobs, especially of CEO/CFO, is to allocate capital. Either reinvest earnings back into the business, M&A, pay down debt/save cash on the balance sheet or distributing it to shareholder via dividends and buybacks. To determine the capital allocation skills you have to review historical decisions. I like to look back 5 to 10 years, take the free cash flow and break down how it was used.

As long as there are reinvestment opportunities that deliver high returns on invested capital management should take these. In part 1 I showed you a excerpt of a Pat Dorsey interview where he talked about reinvestments inside of a companies existing moat which add a lot of value. These are preferable due to the expertise and past execution of management. Chances of high ROIC are simply higher than elsewhere. I will come back to organic growth later.

Beside management could pay down debt or just save up some cash. If debt levels are so high that interest payments really hurt profits or could bring the company in trouble they should pay it down but as debt leverages returns on your own capital it shouldn’t be paid down just for the sake of ‘we are debt free’. Same with building up a cash pile. Sure, some cash is needed for day-to-day operations and gives some flexibility but if managements sits on a large cash pile there are huge opportunity costs.

If the business lags opportunities for reinvestments many managements aim to grow by mergers and acquisitions (M&A). The idea sounds simple: you just buy another business, get access to its knowledge, customer base, products, sales channels and realize some synergies. As I spent some time with serial acquirers I believe exactly that’s the pitfall. The problem is that it is far easier to put numbers on a spreadsheet than it is to actually realize these cost saving or revenue opportunities in the real world. (P. 308). That’s why many M&A deals destroy value. As with capital allocation in general you should look at past acquisitions. To judge these and future ones Michael Shearn focuses on 7 areas here:

Does it fit into the core competencies of the business?

As Dorsey said, we should prefer reinvestments within the moat. M&A within the same industry or same customer base is kind of an investment within its moat. An acquisition outside of competencies may lead to distractions or misconceptions. Which will end in weak operational performance.Does management understand the acquired business?

You want the management to be familiar with the acquired business. E.g. Danaher executives, the famous US serial acquirer, tour plants of potential targets. If you see management thinking they can acquire another company via Teams meetings without spending any quality time with the targets employees, day-to-day operations or the sellers that may be a red flag.

Does the business retain its customer after acquisition?

I talked about customer retention rates earlier. Of course these should stay at a high level after an acquisition otherwise it shows the customers don’t like the deal.

Does the business retain its employees after acquisition?

To merge business cultures is probably the hardest part about M&A. You want to see management is aware of this complicated exercise. For sure there will be lay offs due to realizing cost synergies but nevertheless keeping the key people of the acquired company is really important. They know their customers, their products, the challenges.

Does management have discipline or do they overpay?

The risk in terms of capital allocation lies in overpaying. Overpaying simply destroys value. It’s like buying an overvalued stock. I know, in hindsight it’s easy to judge but there are situations where management may be more likely to overpay: If the company competes in a bidding process, if fear of missing out about a new trend is the motivation behind an acquisition, if management pitches the deal as a ‘transformational’ or ‘game-changing’ one or if M&A takes place in overall bubbles. You want to see a discplined M&A strategy with a clear roadmap about how they approach targets, which price they pay and what happens after acquisition.

Which price was paid?

Evaluate the price. Management should openly disclose what they paid either in press releases, annual reports or separate M&A presentations. You can compare multiples paid to past acquisitions, to M&A deals of competitors in the sector or to multiples of public companies in the sector. The lower the price paid the less the chance of value destruction.

How is the acquisition financed?

Acquirers can use cash, debt or stock. Cash is the most conservative way as the company only uses its own resources. Taking on debt weakens the balance sheet. So keep an idea on coverage ratios. If the business uses stock you ideally do not want the stock to be low valued. The lower the stock of the acquirer is valued, the higher the dilution for existing shareholder and a higher part of the business is being given up to acquire the other business. On the other way around it makes more sense to use high valued stock for acquisitions. You simply give up less of the existing business.

Simply said: you want to have a management team with expertise in M&A deals, proven by successful acquisitions in the past, paying a low multiple and being aware of the operational and cultural challenges while not being overconfident in their ability to realize synergies. Here I want to recommend checking out Learnings from Swedish Serial Acquirers by Partnership Investing.

If all these options seem unfavourable cash should be distributed to shareholders via dividends or buybacks. Buybacks should be preferred over dividends if the stock trades at low valuation where the stock itself offers good expected returns. Valuation is a topic for itself but ideally management got an idea of the company’s value and should be opportunistic about buying back shares. You don’t want to see 100 million in buybacks every year, you want to see 150 while the stock is cheap and 50 million on its way up. Just to give an example. But some businesses just buy back shares to offset dilution so compare dilution with buybacks to see if there is a net effect of buybacks.

Growth opportunities (Chapter 10)

As investing is all about the future cash flows of a business we need to think about how the business looks like in some years. Beside some risks there are always opportunities looking forward. As said before businesses can either grow organically through reinvestments or inorganically through M&A. The ones growing organically focus on their own operation and don’t have to spend time on integration. Some are selective acquirers which acquire to expand their product lines or expand in new markets. Serial acquirers are the ones spending a lot of cash on acquisitions year by year to improve operations of acquired targets and achieve some scale.

Nevertheless through which way a business grows, growth needs to be valuable and sustainable. Valuable growth refers to investing in growth opportunities where the returns exceed the cost of capital. Sustainable growth means a business can grow for many years to come.

To evaluate the overall growth opportunities you can start by reading the reports/listen to calls as management will discuss them. Often they disclose a total adressable market and their market share. But don’t fall for large TAMs here but track how TAM, TAM calculation and market share evolve over time. Recently we saw the Birkenstock IPO on the Nasdaq. Their CEO said their TAM is basically every human being on earth. Even that’s basically true as everyone could wear their shoes, to value the company based on that would be purely naive.

Further you will come across secular growth trends. Basically every business says it benefits from one or another like digitalization or urbanization. Just be cautios not to project high growth for too long. If there is really a secular trend in place that supports long-term growth, the business will face more and more competition. Rather project slowing growth rates and be surprised by stable growth rate caused by management execution than vice versa.

But just growing once for the sake of ‘we are growing’ is the wrong motivation and may be value destroying. If there are limited growth opportunities it’s fine the company mainly focuses on keeping its position in the market and act as a cash cow for its shareholders. Those businesses may not be future ten-baggers but are nevertheless preferable over some unprofitable, high growth, cutting edge whatever kind of businesses. So don’t fall for growth stories where no value is in sight. These may be found in younger companies but also mature businesses may see themselve in a situation to go for risky capital allocation decisions promising to turn the mature business into a growth machine.

R&D

Beside these universal views at future growth it’s important to understand if management is executing here. Especially younger companies or companies which face a lot of competition grow by innovation, by offering new, better, cheaper, … products for their customers. So if you expect the business to grow you need to see R&D expenses that translate into new product which create additional revenue streams. Ideally you find information about how much revenue comes from new products. At this point you could also take a look at margins once more. If there is a new product line responsible for the top line growth but margins are suffering, it’s a sign that growth is not very profitable, at least not compared to the existing business. It may be part of the pricing strategy to attract new customers but it’s something to keep an eye on.

Is the business growing within its means?

This question refers to some structural requirements for growth. Companies should not outgrow themselve and aim for too much. Growth needs to be funded somehow. A business that is taking on high high debt levels or keeps diluting shareholders to fund growth relies on the sentiment of financial markets and can’t operate independently, so is likely worse than a business self-funding its growth over the longer run.

Beside capital it needs the structures to grow. You need enough talented employees to successfully manage growth. Your finance area needs enough accountants for bookkeeping. Your HR team needs enough recruiters. Your R&D team needs enough engineers and your operations area needs enough sales people. Some businesses are more scalable than others but all can’t outgrow their human capital at some point.

Signs of slowing growth

There are many signs of slowing growth but just to get an idea Michael Shearn talks about three of them:

targeting new customer base

changing business models

high dividend payouts

If a business targets a new customer base it’s basically saying that there are limited ways to grow with their existing customer base. Either the business already sits on a high market share for a group of customers, doesn’t know how to attract more customers of that group or sees no ways of up-selling or cross-selling products.

If a business model is changing it also shows that growth is limited. Kind of obvious but management wouldn’t need to change anything if growth opportunites would be in sight.

Sure, both signs also provide an opportunity. If the business attracts a whole new group of customers or successfully transforms its business model it sets the path for valuable growth in the future. It’s just important to understand risk increases if things are changing.

High dividend payout ratios don’t come with an opportunity. Management is basically saying that there is nothing to invest the cash, so here you can have it, dear shareholders. Nothing wrong with that but as said before, these investment won’t be exceptional.

Slowing growth will especially hurt you when you paid up for higher growth. The book doesn’t really focus on valuation but at least here Michael Shearn mentions not to overpay for growth stories. If growth slowes down, companies re-rate. On the other hand businesses who have high upfront investments may mask the underlying cash flows. Here it’s valuable to understand what cash flows look like if investments translate into earnings.

Overall try to understand where growth comes from, how it translates into earnings and for how long it can be sustained. Do not project growth only based on prior growth. Businesses change, industries change, people change, things change.

That’s it for the last part! To sum it up, many topics I, or Michael Shearn, covered would deserve a whole book for themselves. I mean, that’s why there are unlimited finance and business books. Nevertheless I hope this wrap up of Michael Shearn’s book was helpful, catched your interest and may serve as a guide for which topics may be worth a deeper dive for your process.

As said in part 1 Michael Shearn basically describes the perfect business. You won’t find these in the real world. Every business got downsides or yellow flags. That is where valuation enters the game. It may be worth the check out a mediocore business if valuation overstates the risks and that is the one thing I somewhat dislike about the book, or it’s at least what I am missing: valuation. The perfect business is a bad investment if you overpay. Even if you pay a fair price it’s unlikely you end up with exceptional returns. All investing, no matter which kind of strategy, is value investing to some degree. Maybe not in terms of metrics like a low P/B ratio, but valuation always matters.

But all in all the book delivers what it promises. It gives a brief overview on the most important topics, a starting point for your own investing checklist, shows typical pitfalls and where to dig deeper.

I have to say it was tougher to write this than expected as the book covers so many topics that it’s hard not to lose myself in details while also not keeping it too simple. Would appreciate any kind of feedback on these three parts.

Thanks for reading!

Cheers.