Part 1: Uncovering opportunities and business foundations

Part 1: Uncovering opportunities and business foundations

Book summary: The Investment Checklist - The Art of In-Depth Research

Especially as a beginner you often don’t know where to start. You look at one company after another without any structured framework. As time goes by and you learn which characteristics you want to avoid and which to look for. However, as your knowledge grows, so does the number of questions in your mind.

That’s why I decided to read: The Investment Checklist by Michael Shearn.

The purpose of The Investment Checklist is to help you implement a principled investing strategy through a series of checklists. In it, a thorough and comprehensive research process is made simpler through the use of straightforward checklists that will allow you to identify quality investment opportunities. Each chapter contains detailed demonstrations of how and where to find the information necessary to answer fundamental questions about investment opportunities.

Michael Shearn goes through 59 questions from understanding the business and its financials up to management quality and future growth opportunities, explains why it matters and what to look for. He basically describes the perfect business. You won’t find many businesses that check all the boxes but I guess it’s helpful to understand which characteristics would make up the perfect one.

Some questions are fairly basic while others require more knowledge of the industry. Most answers you will find in annual reports, management discussions, earnings calls or by talking to IR. He provides some sources on where to find information but as some are just useful for US companies and rather helpful for looking at large caps I won’t focus on them. Best way to answer them would be to talk to management, customers, suppliers or employees and if you have the chance to get that detailed information go for it. But as a private, non full-time investor it’s more important not to lose yourself in details. You’ll reach a level of detail where more research probably doesn’t add anything to your returns. I don’t believe investors need to answer all questions in detail, but it’s worth considering them during your research.

I would say the book is mainly for investors who already got started but need a wrap up of all the thing they came across with some new insights. Further research on most topics is likely needed as the book gives more of an overview and explains the most important concepts of a topic but doesn’t dive too deep. So for really experienced investors it’s probably more of a overall refresh, for less experienced ones it provides some starting points for diving deeper.

In terms of investment strategies the book fits a quality/compounder, long-term/coffee-can approach the best but is helpful nevertheless if that’s not your way of investing.

Overall I will not go through this book question by question and won’t strictly stick to the books structure but will share overall takeaways from each part of the book mixed with my own takes, more or less describe the perfect business and recommend to read it yourself if you get interested.

I’ll split this into 3 posts:

Part 1 covers finding ideas and understanding the business in general.

Part 2 focuses on its financials and the management team.

Part 3 takes a look at capital allocation and growth opportunities.

Let’s start.

How to generate investment ideas (Chapter 1)

‘You can’t manufacture investment opportunities.’ (P. 1) - to start with a quote. According to Shearn you first of all need to be patient and prepare youself for opportunities. As we know most stocks are bad investment. Returns of the broad market are attributable to a small basket of companies with outstanding returns. That’s why we shouldn’t try to ‘manufacture’ investment ideas. I would even say investors can manufacture ideas, but not good ideas. If you catch yourself trying to like a company or trying to hit your expected IRR by changing inputs in your financial model, you are manufacturing.

But there is no need to. Investment opportunities probably occur every day, somewhere, due to forced selling, fear, overreactions, uncertainity, … . We can’t be aware of every opportunity out there but we can use tools to help us find some of them. Michael Shearn recommends:

Stock screeners to help us find stocks that fit your personal investment criteria

New-lows lists to find stocks that do not deserve the stay low

Newsletters, media recommendations, overall business press … all kind of journalistic sources

Upcoming IPO’s or spin-offs

I would add Fintwit or social media in general nowadays. You can also set up mail alerts e.g. in Quatr or Google, for buzzwords like spin-off, buybacks or whatever interests you. Every source got its weaknesses so be aware of not just buying a stock because it appeared in your source.

Shearn does not recommend to follow successful investment managers because a lack of transparency, changing strategies and their mistakes you would copy. I agree in terms of not copying others e.g. as we see every quarter when Buffett discloses his trades and all the headlines are flooded with his trades. But nevertheless there are many smaller investments funds out there pitching their ideas (Here is Tweet by

with some great fund letters, ToffCap is a great source by itself too).But simply because you come across a pitch, don’t stretch your investment criteria. It’s more important to say ‘no’ quickly than trying to understand every business. That’s why Shearn also recommends to establish overall critierias no matter if financials, industry, the kind of product, … . Of course it takes time to find criterias but as you learn, or read this book, you will find characteristics of businesses that serve as a green or red flag for you personally.

However you don’t have to look for new ideas. Don’t forget what you already own or owned in the past. The best ideas for you maybe those you already own and know. That’s why Shearn recommends to ‘create an inventory of ideas to track potential investments that meet your criteria on a continual basis in order to prepare for future opportunities’ (P. 20). If a business doesn’t fit some of your critieria yet e.g. due to high valuation, debt levels, new management, … it could be worth to do some work on it nevertheless, keep it on your watchlist and come back later. Especially valuation is a ‘pass for now and come back later’ kind of filter.

Understanding the business (Chapter 2 & 3)

Michael Shearn splits this part in two chapters: the basics and the customers perspective.

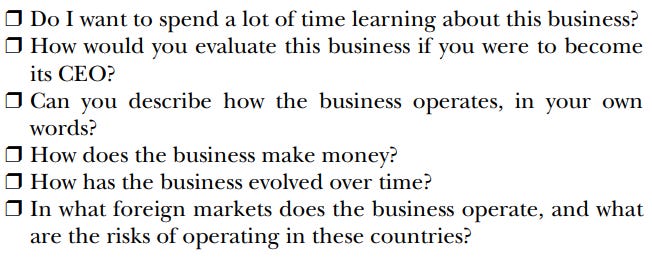

Chapter 2 covers some more basic questions like how does the business make money or what to learn about its history. Nevertheless it’s an important part of your process. Not understanding what the business is doing may lead to misjudging or poor decision making when the stock moves. So keep in mind you don’t get any credits for digging into the most complex business models. If you can’t wrap your head around it, admit that you don’t get it and pass.

Before even spending time on the business itself ask yourself if you even want to learn about this business. As a private investor we look at companies in our free time, many would say it’s a kind of hobby. So be aware that even if there is a nice pitch, it’s not for you if you are bored and distracted while digging deeper. A hobby should be fun. But on the other hand, your personal preferences may shape your view on a company. So just because it’s fun to look at it, it doesn’t need to be a good investment.

A mental model Michael Shearn uses in the book is ‘How would you evaluate this business if you were to become its CEO?’. I like that way of thinking. Ask yourself what you would want to understand about the business if you had the opportunity to join it. E.g. the business segments, who are the customers, who are the key people, competitive advantages, R&D pipeline, headwinds, tailwinds, risks, history … and try to work through topics that seem important to you. Some of these are discussed in more detail in following chapters. You will learn the most by reading a businesses reports, maybe you find interviews of insiders online or know people who got a deep understanding of the industry/business.

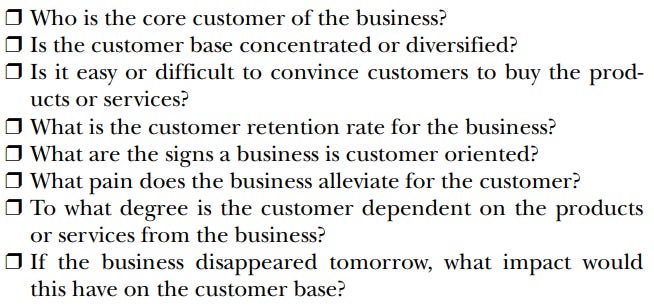

‘The quality of a business is determined by the quality of its customers’.

Take a look at the number of customers and customer concentration, which can be a source of risk. The more customers, the less dependent the business is on a single one. Further evaluate the importance of the business for its customers. Indicators are customer retention rates or sales tactics. High customer retention rates show that a business is retaining its customer rather than churning them. These can be improved by building long-term relationships and investments into customers, e.g. loyalty programs which in best case lead to up- and cross selling opportunities. Especially subscription businesses tend to disclose their customer retention rate. In contrast, high-pressure sales tactics (like buy it now or lose the opportunity) can be a sign of unsustainable customer relationships. It’s probably easier to evaluate for B2C than B2B businesses but look for ads of the business to see which way of marketing they use.

Further try to take on the customers perspective to identify the problems that are being solved by the business for the customer. E.g. a pharma business is alleviating the pain of a disease so it’s crucial for the customers life quality. In best case the products/services are need-to-have’s rather than nice-to-have’s. But since someone has to pay for the products think about the solvency of customers. If the price of the product/service make up a small portion of the customers wallet and is crucial for them it leads to less volatility in demand. Nevertheless be aware that just because products seems to be nice-to-have it doesn’t mean sales are volatile in tough times. Building competitive advantages which is topic of Chapter 4, such as a successful brand may, lead to resistance vs economic cycles.

Strengths and weaknesses (Chapter 4)

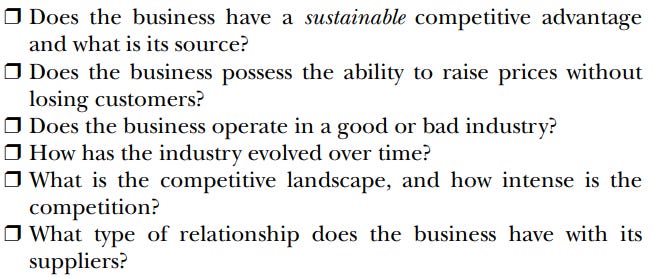

If we invest for the long-term, we need to identify companies in a strong competitive position, enabling them to sustain current earnings and foster future growth. These companies are simply more valuable. Here, it’s important to understand that a strong competitive advantage differs from a sustainable one, as unsustainable advantages can be copied or disrupted, leading to the loss of the company's edge.

Sources of sustainable competitive advantages are network effects, intangibles like brands, patents, regulatory licenses, switching costs for customers or cost advantages. Each of these comes with different KPI’s an investor could track over time to assess their sustainability. For example, high customer retention rates can be a sign of high switching costs for customers and/or a strong brand. High margins compared to competitors can be a sign of cost advantages. Stable or increasing gross margins despite fluctuating input prices, without losing customers, indicate pricing power. Advantages supported by regulatory licenses or patents require knowledge about the process for obtaining them, their duration, the involved authorities, and potential business impacts if circumstances change. In best case moats are structural as these are harder to copy. To retain a successful brand the company relies on consistent management execution while an advantage such a great location for a distribution center is more persistent by itself.

But even the greatest moats need to be defended. Companies need to invest in their product/services to keep their competitive position especially in emerging industries. So ideally you want to find companies that are increasing their competitive advantages by investing in their core business. Michael Shearn shared an excerpt from on Interview of Pat Dorsey on reinvestments inside and outside of existing moats.

The interview took place in 2011. Interesting to note that Microsoft was seen as a mature business with limited growth opportunities. As we know today Microsoft’s investments outside of their existing moat built a new moat around their second core business: Azure.

But before looking at strengths and weaknesses of a particular company it might be worth looking at the overall industry first. If an industry tends to be cyclical, if competition is tough (increases customers choice and costs), if it’s constantly changing (hard to predict), if it faces overall disruption, if ROIC is low on average, … that may be signs that you don’t even want to look at any company operating there which can become part of your initial criteria. But if you enjoy researching a particular industry, learn about it and you will find opportunities even if it looks uninteresting at first.

Ideally you look for an industry with limited number of competitors, facing long-term tailwinds with high average ROIC, which shows that it’s easier to make money here. You can compare the best and worst businesses based on KPI’s to understand what makes some companies unique and why others suffer. Just be aware that industries change over time due to foreign competition, new trends or others. A suggestion from Michael Shearn that I find valuable is to search for articles about the industry's history and study competitors who have faced challenges or even failed to learn about potential threats to your business.

As we talked about customers earlier, which can be a risk for a business if there is customer concentration, same goes for suppliers. You need to determine if there is any supplier concentration, how price increases impact the business and if the business has access to reliable sources of supply by valuing long-term relationships with suppliers, … . If there are long-term contracts which secure access to resources management will likely point that out, so if not it may be worth to dig deeper here and send a mail to IR. Management should see its suppliers as partners, probably even collaborates based on customer feedback rather than squeezing them for higher margins.

That’s it for part 1. Especially moats would deserve their own post. If you would like to dig deeper here it could be worth to look for work of Pat Dorsey or Michael Mauboussin (Link to his paper on moats).

As said before i didn’t necessarily stick to books structure. I skipped some questions and just talked about the stuff I found to be useful. If you got any kind of feedback let me know!

Here you can continue with Part 2 where we look at chapters 5-9: financials and management teams, inevitable for succesful investing.

Thanks for reading! Cheers.