Part 2: Financials and Leadership – The Backbone of Success

Part 2: Financials and Leadership – The Backbone of Success

The Investment Checklist: The Art of In-Depth Research

This is the second part of my wrap up of Michael Shearn’s book The Investment Checklist. In the first part, we looked at broader aspects of the business. Now, we shift our focus to the financials and gaining insights into the individuals running it.

The financials (Chapter 5 & 6)

No matter how promising a business may seem qualitatively, its true potential is revealed in numbers. If the qualitative strengths aren't reflected in the financials, it could signal a risky long-term investment. That’s why chapter 5 focuses on the operating and financial health.

Top line

Ideally, you favor businesses that generate recurring revenue models such as a subscripton-based service as those revenue streams increase predictability of future cash flows and mitigate volatility. Particularly, if the product/service is a need-to-have it helps avoid the risk of fluctuating earnings during economic cycles. So as you research a business consider how its top line evolves, which economic conditions make it easier for the business to be successful and look at past recessions to understand how demand may have shifted.

Costs

In general, businesses with a high fixed cost basis will suffer more from declining sales as it’s harder to reduce costs to keep up margins. Michael Shearn recommends to compare fixed assets to total assets or to categorize costs on the income statement in fixed and variable costs to identy to what degree a businesses earnings are impacted by operating leverage. Another disadvantage of high fixed costs are high capital expenditures to maintain them. The more cash needs to be spent on capex, the less cash flow is available for reinvestments or distributions to shareholders. But not all capital expenditures you find on a cash flow statement are necessary to maintain assets. If possible, you want to separate maintenance and growth capex. Growth capex are new investments to generate excess returns in the future, while maintenance capex only serve to keep the company at a stable level. Alongside keep an eye on when assets need to be replaced as this results in higher capex. For example we know airplanes are replaced every 10 to 20 years and buying a new airplane is more expensive than maintaining an old one, at least initally. To determine when assets could be replaced compare net fixed assets to gross fixed assets. The closer the ratio is to 1, the lower the risk of higher capex due to replacement of assets.

Key performance indicators

But to be successful management needs to execute on its most important operations. It’s not enough to simply grow revenues or keep margins as high as possible at any cost. Netflix has to produce entertaining shows or Chipotle has to serve good food. That’s why we track KPI’s (key performance indicators). Sometimes it may be tough to track KPI’s like if the average show is entertaining but if they wouldn’t, it would be seen in a KPI like customer retention rate. There is probably an unlimited number of KPI’s but typically management discloses some in reports/presentations like same-store-sales for a retailer, costs per …, revenue per …, number of employees/locations /customers. Track these KPI’s that provide information about the underlying business over time, compare them to competitors and find out why, if they differ or change.

Inflation

But as we invest for the future it’s not enough to track KPI’s which tend to be a look backward. The future comes with uncertainty about risks. I talked about that in terms of moats already. A main risk every business faces is inflation. The cash flow of a business has to increase in line with inflation to avoid a value destroying effect. Due to higher inflation right now we can perfectly observe how different businesses handle inflation: some suffer, some even benefit due to price increases that remain when costs come down. Especially these businesses with pricing power and low fixed costs will do well in inflationary times. The annual reports of the last 3 years will be great case studies on how particular businesses are effected by inflation. Also watch out for refinancing risk. Even though higher inflation may benefit businesses that carry a lot of debt, it may harm them if there is need to refinance their debt due to higher interest rates in inflationary times. So all in all it’s important to understand which cost increases impact the business. For example REIT’s suffer from rising rates, professional services from wage inflation or airlines from rising fuel costs.

Debt

As we talk about debt: some businesses carry higher debt by nature as REIT’s but generally a strong balance sheet (low debt levels, cash reserves), gives management the ability to be opportunistic about future investments and overall strategic decisions. If there is debt determine if the business is able to handle by looking at coverage ratios as debt/EBITDA, debt/assets, cash flow/interests and why there is debt: to fund losses? growth capex? fund M&A?

Moreover don’t overlook non-bank-debt like lease liabilities. I am far from an accounting expert and I know there are accounting standards where you would double count leases by threating them as debt, as lease expenses are included in operating costs, but you could see this as conservative approach to generally include them if you are unsure.

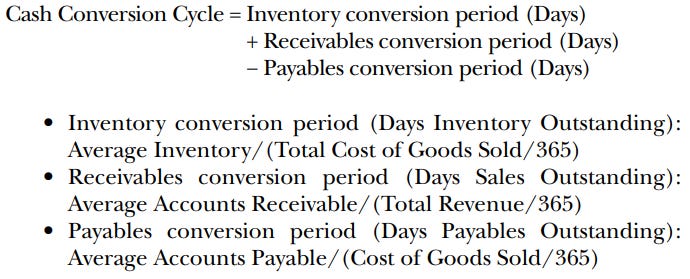

Working capital

The balance sheet also provides information about working capital. Wc is the cash needed to fund day-to-day operations. By better managing working capital a business can free up cash that would otherwise be tied up, which leads to opportunity costs. Beside thinking about wc as % of sales or look at the overall change in working capital you should calculate the cash conversion cycle (CCC) which shows the number of days cash is invested in investories and receivables:

Michael Shearn recommends calculating the CCC for at least a 5 year period to understand if and why the CCC is changing. If changes are temporary for CCC, which impacts working capital, you would have to normalize cash flows for these effects when predicting cash flows.

Working capital can be negative, often seen in growing SaaS businesses, which means customers and suppliers are financing the business as they allow you to defer payments and use the cash otherwise. As long as a business is growing this works perfectly in its favor, but if growth stops these positive effects will reverse and decrease cash flows as the business can’t defer liabilities further into the future.

ROIC

Working capital is also part of ROIC (Return on invested capital). The basic idea is that a business with higher ROIC is considered a higher-quality business as it requires less capital to achieve the same returns. There are multiple ways to calculate ROIC but I prefer using operating profits (EBIT +- adjustments) divided by invested capital (wc + non-current assets +- adjustments) and personally recommend to read the work of Michael Mauboussin on ROIC to learn what kind of adjustment you could do (link to his work on ROIC). As far as I can tell there are no big differences of Michael Shearn’s takes on ROIC compared to Mauboussin’s but he covers ROIC in more detail. That’s why i refer to him and more or less skip the part in the book here.

Accounting standards

As we look on the income statement, cash flow statement and balance sheet we learn about the business based on accounting standards. There are accounting rules like GAAP or IFRS but nevertheless management is able to influence if these are used in a conservative or liberal manner. Michael Shearn pays attention to the most common signs of manipulated or overstated earnings. Things that should set off some alarm bells:

If a company is reporting earnings but yet not paying taxes

If net income is consistently higher than operating cash flow

If financial statements are too complicated in general

Inflating sales: accounts receivable grow faster than sales

Under- or overstating expenses: Current expenses are defered to later periods either by capitalizing them which makes them appear on the balance sheet as assets or by cutting discretionary costs out of nowhere e.g. just to hit an earnings target

Changing accounting methods: e.g. extending the useful life of asset to lower D&A which boosts earnings (Waste Management restated financial statements in 1997 after their prior CEO used this method to boost earnings)

Restructuring charges: if managements report a restructuring loss, they may add extra expenses into that to decrease future expenses. Additionally they can boost future earnings when reversing the liability if they overestimated restructuring charges

Using reserves: management can over reserve in good times and then cut back or even reverse charges in bad time to boost earnings, so look if reserves match actual write offs

Of course these signs doesn’t mean its a fraud but you probably should dig deeper here on why things are as they are and question managements integrity if there are no explanations.

Management (Chapter 7, 8 & 9)

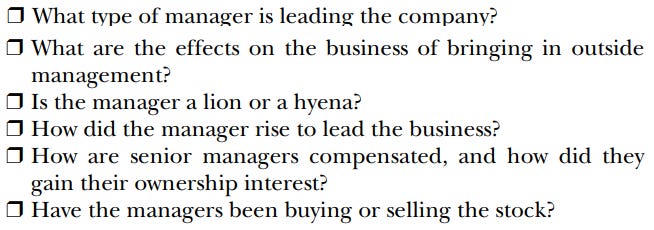

The relations to customers, the quality of products or the methods of accounting are directly tied to the quality of a businesses people. Especially in the long-term you will rely on managements execution, so you should try to gain insights into their character. As you try to understand what drives value for the business, management should too. To determine which type of of manager is leading the company Michael Shearn uses a classification system: OO, LT or HH.

OO stands for owner-operator. He further breaks it down into 3 types of OO’s.

Owner-operator 1 (OO1) is the best manager to partner with, typically the founder. As they put all their hard work into the company they take on a long-term view, want the business to be successful, serve all their stakeholders and often have high insider ownership.

Owner-operator 2 (OO2) is not a founder but nevertheless passionate about running the business. Typically receives a higher compensation packages than OO1.

What differs Owner-operator 3 (OO3) from OO2 is a manager who runs the business for their own benefits. Nevertheless passionate but you will see even higher compensation packages and related-party transactions. Shareholder value may not be their priority.

LT stands for long-tenured manager, someone who has been in the industry for many years.

LT1 are the ones who are with the business for a long time and have been promoted from within the business.

LT2 have joined the business from outside but worked in the industry for many years. They served a similar customer base and know how to operate a business in that industry.

But be aware that someone who has spend his career in the corporate suite, like a controller, may not fit for a job like CEO, which is way closer to operations and customers.

HH stands for hired hand and is someone who recently joined the company and is not from the same industry. These tend to jump from job to job (look at their cv) and are focused on the short-term.

HH1 joined from a related industry

HH2 joined from an unrelated industry, so has no experience in serving the customer base

Ideally, you want partner with managers who are in place for a long time with a proven track record. If management teams change, the past financials offer less insights for the future. Of course a change in leadership team isn’t a red flag, that’s life, but it comes with risks.

Also be aware that it’s really hard for successful managers to replicate their success in a new business. Beside their own capabilities, factors like their internal network, resources or unwritten rules and behaviours impact the results of their work. There is a study called ‘The risky business of hiring stars’ where the performance of 1000+ stock analysts was observed. It showed if ‘star analysts’ were hired by another investment bank their performance plunged due these factors I mentioned. Don’t want to overgeneralize the results but good to keep in mind.

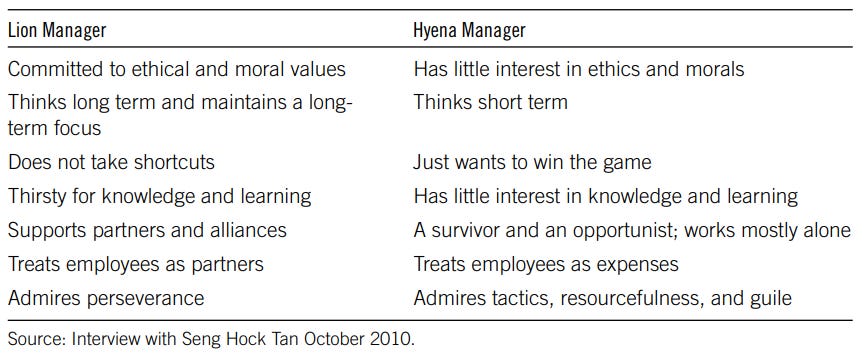

Further Shearn recommends to separate if a manager is a lion or a hyena:

As you can guess by looking at the traits you want to partner with a lion in the long run. Sure it’s hard to judge but by reading articles and following their actions over time you may be able to determine if someone is rather a lion or a hyena.

Compensation

Money is an external motivator and here you learn a lot about the manager. You want to look for managers with passion, not someone who is motivated by the next paycheck. Nevertheless all managers get paid. Watch out for high fixed compensation or large variable compensation only for the c-suite based on non-operational performance like the stock price. Ideally you look for low fixed compensation and variable compensation based on long-term operational performance. Further it’s a good sign if variable compensation such as stock options is offered to all employees as it shows employees are seen as partners who are allowed to participate if the company is successful.

Insider ownership is not part of the compensation but gives the same incentives as variable compensation. As management holds shares of their own company they are more likely to act in favor of shareholders.

In terms of insider trading I wouldn’t spend too much time on it. If insiders add to their stake it’s seen as a good, if they sell as bad. As there are many reasons for insiders to trade their shares buys only matter if it’s a notable amount of their net worth, sales only matter if combined with other warning signs. Otherwise they are mostly noise.

Communication and passion

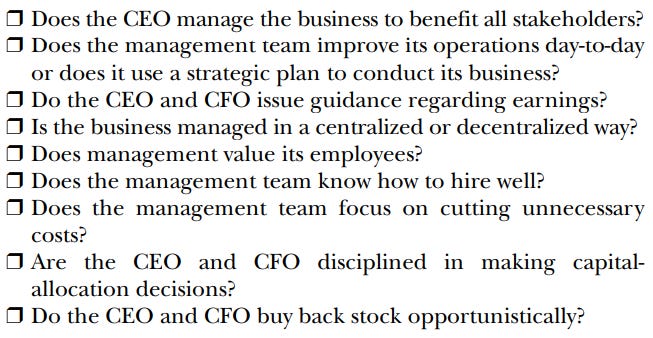

Beside the type of managers and their compensation, what really matters are their day-to-day actions and how they operate the business. That’s why focussing on their execution is important. Even though we care about the shareholder value as a shareholder that probably shouldn’t be the no. 1 focus for managers. Shareholder value is the result of happy employees and customers so don’t fall for managers who fail to understand their job to balance all stakeholder interests.

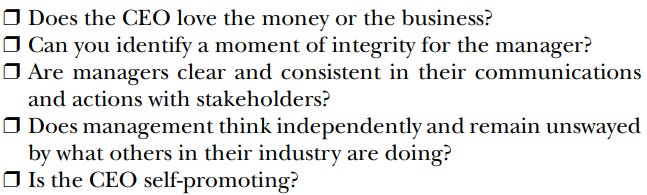

In normal times it’s probably the hardest to judge a manager. Where passionate managers differ from unpassionate ones is in difficult times, when they feel pressure. Latter will blame others for weak performance, only think about the short-term and evade difficult questions. You want to look for integrity, for actions following their words, for admitting mistakes, for live-long learners, for honest and straight communication without corporate bla bla, for humble people. As I said before: hard to judge, so keep your eyes and ears open and monitor managements actions over time.

Guidance and long-term plans

I’ve always appreciated it when management provided guidance but as I had some discussions on the topic I noticed that it’s probably more or less noise. Michael Shearn adds strategic plans here. He says businesses are built based on many many small decisions every day and not by a strategic plan. When managers think one strategic decision like a large M&A deal will transform their business, it may be a warning sign. Don’t fall for these plans. Henry Singleton, CEO of Teledyne, believed no plan was the best plan: ‘we’re subject to a tremendous number of outside influences, and the vast majority of them cannot be predicted. So my idea is to stay flexible. I like to steer the boat each day rather than plan ahead way into the future.’ According the Shearn these plans fail as they limit your flexibility and create pressure to execute these even it may not be the best for the business anymore. Especially financial targets often set the wrong priorities and ignore that businesses don’t grow in linearity. As with most topics in the book, a guidance or strategic plan is not a red flag but try to determine what’s the motivation behind it, examine past guidances and assess whether management delivered on them.

Management of employees

‘The primary function of a manager is to obtain results through people.’ (P. 225) Michael Shearn recommends to start with determining if management uses a centralized or decentralized structure. In centralized structures you see top-down hierarchies, lot of bureaucracies or limited flexibility in decision making which may lead stressed, unhappy employees who are not committed to the business. In contrast, employees in decentralized structures are empowered to make decisions which makes them feel valued and trusted by management. This kind of structure/culture attracts new employees by itself and makes it easier to hire great people. So based on the structure look for signs where managements truly values their employees e.g. by promotions, by not laying them off in tough times or by investing in employee training. Happy employees will make happy customers. Employees should have to ability to speak up, to present new ideas and to be, as I said before, a partner of management. Signs for that could be awards like ‘Best place to work’ or low employee turnover which results in lower hiring costs and better customer relations. Also look for low turnover in the c-suite and board. A high turnover makes it harder to build a successful business in the long run. As we talk about the board you should take a look at who the CEO is bringing to the board. If you see a CEO filling it with friends or politicians that may be a warning sign. You want to see directors who offer value for the business due to their expertise and care about the business and its shareholders.

That’s it for part 2. These both topics are probably the most important ones for successful investing so I hope I could give provide a brief overview on them.

As said before i didn’t necessarily stick to books structure. I skipped some questions and just talked about the stuff I found to be useful. If you got any kind of feedback let me know!

Here is part 3 where we look at chapters 10 & 11: capital allocation and growth opportunities. Capital allocation is part of chapter 8 but as chapter 11 covers M&A I decided to combine them.

Thanks for reading! Cheers.