AIM A-Z Part 18: Cheap Distribution and Solid Professional Services

Ticker 321 to 340 on London's Alternative Investment Market (AIM)

Welcome,

a part with ups and downs today. Fight through the pre-revenue mining companies and you’ll find two solid professional service companies, two distributors (one of them on my watchlist) and some other companies that may be worth a look for some of you. Let’s go!

Here you find the last part:

Here you find all other parts: https://increasingodds.substack.com/s/a-z-uk-aim

321) KCR Residential REIT (Ticker: KCR)

5£m residential property company. Share price jumped 50% in June after a group of shareholders wanted to replace all board members at the AGM. But the resolutions failed as only 15% of shareholder voted in favor. Share price didn’t crash back to old levels afterwards. Torchlight Fund owns 55% of shares. Acuity RM, which was part of the A-Z already, owns 5% (they provide risk management software), no insider ownership.

Fundamentally, the business is struggling: about 1,8£m in rent income but negative operating cash flow. Focused on reducing cash burn. Refinanced their debt with a 6% interest rate (up from 3,5% before), which will increase debt costs by 0,2£m a year. NAV ~13£m, but there are no plans to liquidate assets apparently. Pass.

322) Kefi Gold and Copper (Ticker: KEFI)

118£m no-revenue gold exploration and development company with projects in Ethiopia and Saudi Arabia. Share price 3x on positive project updates. Pass.

323) Keras Resources (Ticker: KRS)

2£m unprofitable operator of a diamond dreek organic phosphate mine in the USA with additional interest in an ore mine in Togo. Reduced cost base and highlights positive development in H2. Pass.

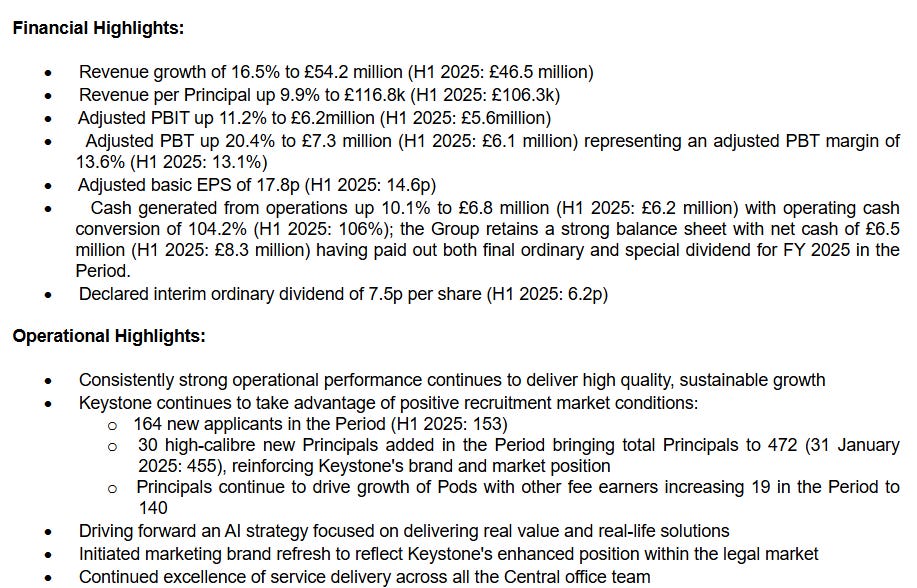

324) Keystone Law Group (Ticker: KEYS)

222£m legal service company operating a platform for self-employed lawyers where lawyers and KEYS share received fees.

Growth driven by more lawyers. Expects adj. PBT for FY26 to be above 12£m. Is lead by James Knight who founded KEYS in 2002 and owns 28% of shares. 22x fwd. P/E (Koyfin). As said before in this series, I struggle to find professional service businesses interesting (from a personal-motivation perspective whether looking into them deeper or not) so I pass here as well. But I want to recommend the write-up by @Bastiaan, it’s nicely written and great to understand the business model despite being three years old:

325) Kibo Energy (Ticker: KIBO)

1£m developer of thermal coal power projects in Africa. Suspended trading since April 2024. Pass.

326) Kistos Holding (Ticker: KIST)

134£m unprofitable ‘energy company with upstream and midstream operations across international markets’. Operating in the UK, Netherlands and Norway. CEO owns 17%. Pass.

327) Kitwave Group (Ticker: KITW)

198£m groceries wholesale business that I have on my watchlist already. 22% insider ownership. The elevator pitch here is that it’s a slow grower (<5% yearly organically), with a M&A track record (>10% growth annually) suffering from short-term headwinds (national insurance hike, weak leisure market, delayed M&A integration) while being cheap compared to competitors after a profit warning. Management still expects 38£m to 40£m in adj. EBIT → EV/adj. EBIT ~ 7. I just recommend to read the work of Jon Curkierwar from Sohra Peak Capital Partners.

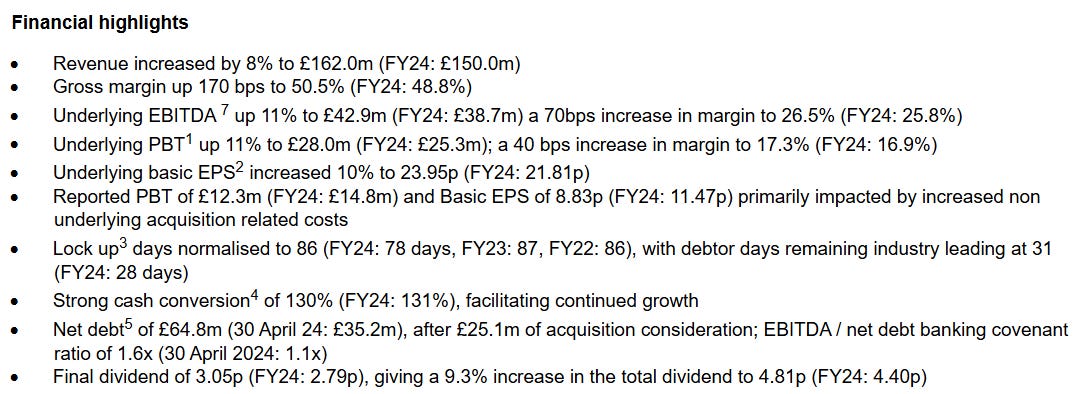

328) Knights Group Holdings (Ticker: KGH)

172£m legal and professional services business. Recent results looking strong:

Growth driven by M&A, client wins and recruitment. Did another 25£m acquisition after the reporting period. Expects further profitable growth in the medium-term based on the same growth drivers. CEO joined in 2011 to restructure the business and owns 22% of shares. Grew revenues and adj. PBT by over 15% a year since 2020. 65£m net debt. Trades on ~7,5 EV/adj. EBIT. Most services related to real estate, private wealth and dispute resolution. Even though KGH looks solid (as most professional service businesses), I pass again. I do not agree with all their profit adjustments and the M&A deals require a deeper look as goodwill is their biggest asset.

329) Kodal Minerals (Ticker: KOD)

59£m no-revenue company with interest in an African lithium project. Just received an export permit in Mali. Pass.

330) Kooth (Ticker: KOO)

51£m company focused on ‘youth digital mental wellbeing’, means they provide services to enable people improving their mental health. Recent results show flat revenue, but -80% adj. EBITDA and net unprofitability due to ‘front-loaded’ 7,2£m investments in marketing in California and because 2024 profits were not considered sustainable anyway. Expects ~9,5£m adj. EBITDA for FY25. 15£m net cash, just completed a 1,5£m buyback programme. 95% of revenue is recurring. A venture capital guy on the board owns 26%, CFO joined Kooth from his VC company. Pass, also because of issues highlighted by @Just A Value Investor :

331) Kore Potash (Ticker: KP2)

177£m no-revenue mineral exploration and development company with a project in the Republic of Congo. Listed on AIM, in Australia and South Africa. Pass.

332) KRM22 (Ticker: KRM)

15£m provider of risk management software for capital market companies. 90%+ revenue recurring, operating unprofitable but is confident ‘to become a cash generative and profitable business’. Balance sheet looks ugly with net current liabilities of 8£m and non-current assets consisting of only intangibles (goodwill and development costs I assume), seems risky for a risk manager. Pass.

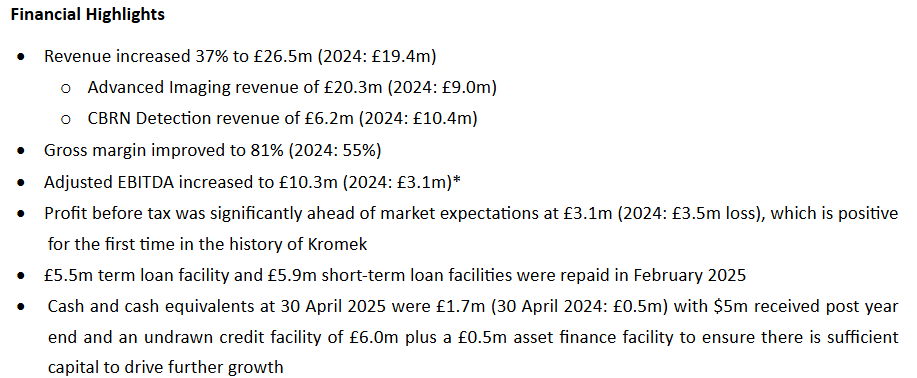

333) Kromek Group (Ticker: KMK)

41£m manufacturer and provider of hard- and software for radiation detection. Results looking strong, but this is mainly due to an agreement with Siemens to supply parts for certain applications.

Contract volume of 37,5£m, KMK received 25£m already, betting on follow-up orders could be the case here. Is also dependent on government contracts in the US and UK. Expects to grow profitable in 2026. Interesting niche for sure, but one contract makes or breaks the year I assume. Questionable whether profitability is sustainable. Pass.

334) Kropz (Ticker: KRPZ)

8£m plant nutrient producer with a phosphate mining projects in South Africa and Republic of Congo with negative gross margin. Pass.

335) Landore Resources (Ticker: LND)

13£m no-revenue gold exploration and development company operating in Canada. Drilling tests ongoing. Pass.

336) Lansdowne Oil & Gas (Ticker: LOGP)

1£m no-revenue O&G company. Suspended from trading since March 2024. Pass.

337 - 338) Latham James (Ticker: LTHP / LTHM)

213£m distributor of timber, panels and decorative surfaces. Flat revenues YoY and EBIT down to 20£m (from 26£m), partly due to a 2,5£m one-off pension charge. A main competitor filed for administration recently. Latham plans to build a national distribution center for 45£m (6£m land + 39£m property) to defend their market leading position, purchased their leased site in Scotland and will implement a new warehouse management software on all sites over the next years. Market Cap = NAV. Revenue peaked in 2022 (I assume due to inflation) and is more or less flat since then. 5,5% dividend (2/3 is a special dividend). Latham family owns 15%. 11x fwd. P/E (Koyfin). Solid business, but also not too interesing. New distribution center will take 2-3 years to build. Pass.

339) LBG Media (Ticker: LBG)

206£m digital publisher through social media platforms and own websites, makes money with marketing services for blue chips and ads on its own profiles/websites: some may now Unilad or LADbible. H1 25 shows 13% growth, highlights growth of clients with >1£m revenue (17 now, 7 in H1 2024), so there is some little customer concentration among blue chips. I burned my fingers on ad businesses after covid, making me biased and not finding myself being interested.

CEO is the founder of LADbible and owns 42%. Co-Founder of Boohoo Group (AIM-listed, fashion group) is on the board as well. Fwd. P/E of 14 (Koyfin). If one wants to bet on rebounding consumer sentiment, especially in Gen Z, LBG is definitely worth a closer look. I pass here.

340) Lendinvest (Ticker: LINV)

55£m unprofitable asset management platform for real estate. Shifting to a capital light model, with 79% of assets managed on behalf of third parties. 3£b assets under management, 22£m fee income, 16£m interest income. Reduced headcount by 15%. Co-founders (both own 28%) are still involved, CEO joined in 2015. Complicated, pass.

Wrap-up

340/669 companies covered so far.

Watchlist: 46/340.

Pass: 294/340.

No-Revenue counter: 78/340.

Feel free to provide opinions and sources on any of the stocks. Cheers.

Thanks for these AIM writeups a really useful and interesting exercise.

James Latham - the peak revenue in 2022 caused by shortage in timber supply (logistics disruption) and spike in prices - Lathams long term supplier relationships allowed them to maintain supplies. Since then prices have been normalising (according to the director commentaries). The liquidation of a competitor caused lower prices in the short term as the administrations sold off stock - but is expected to benefit Latham in the longterm.

Storing timber is a bulky business. Can't be ordered 'just in time' and at best prices. Latham distribution sites are well located for the trade but can't easily expand - the NDC looks expensive but will allos Latham to handle timber stock more efficiently optiimising buying price and reducing stock held at each site - and allowing range of stock items being sold to be increased. Increasing the prospective turnover and profit of each site.

Or that's the plan. Will it be a white elephant. There has to be a risk. With a 250year history the founding family is not given to aggressive risk taking? Management is usually cautious and the NDC looks to be a big step for them - my assumption is that management are intent on doing it right. Buying the land and funding from cash helps to reduce the risks even if it lowers the financial efficiency?

I held the shares during the climb from around £1 to £10 a few years ago - though with an undersized position. I don't hold them now - but they are in an ISA that I manage. As a sleep at night share. I rate the management and will probably be a steady eddie compounder from here?

cheers

Mark (Illiswilgig)

https://illiswilgig.substack.com

That would be great thanks.

J