AIM A-Z Part 17: Quality Serial Acquirer, Special Situations and Public Transport

Ticker 301 to 320 on London's Alternative Investment Market (AIM)

Welcome to part 17,

today we go through a mix of everything: pre-revenue to quality, mining to commercial flooring, micro cap to mid cap. Two for my watchlist that I’ve known before. Two special situations. Two solid public transport companies. Let’s go.

Here you find the last part:

Here you find all other parts: https://increasingodds.substack.com/s/a-z-uk-aim

301) Iomart Group (Ticker: IOM)

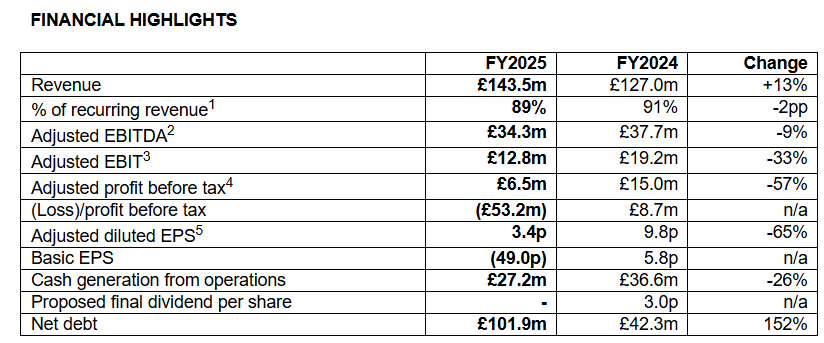

18£m provider of cloud managed services (infrastructure, workplace management, security). Apparently focused on Microsoft’s Azure and Broadcom’s VMware cloud. In October 2024, Atech was acquired 57£m (about 50% of IOM’s market cap back then), an unprofitable Microsoft partner.

FY25 numbers include a 53£m goodwill impairment related to their ’Cloud Services Cash Generating Unit’ due to customer churn. Adjusted profitability down due to Atech and the churn. The adjustments are mainly related to the impairment and amortisation of acquired intangibles, what I consider to be fair adjustments to reflect underlying profitability. Atech contributed for 6 months. Net debt about 4x operating cash flow.

For FY26 management expects cost savings of 4£m and saw net positive bookings in Q1 already. Gresham House Asset Management increased its stake in IOM from ~20% to ~30%. I’d expect less adj. EBIT here for FY26 when Atech contributes for 12 months. The net debt is a burden and the impairment requests a closer look on capital allocation decisions in the pasts. Pass.

302) IQE (Ticker: IQE)

76£m supplier of compound semiconductor wafer products, apparently a market leader in its niche. Suffering from macro headwinds, unprofitable. Strategic review ongoing: ‘The Board is now expanding the scope of the previously announced Strategic Review to also incorporate the potential sale of the Company and is seeking buyers.’ No matter the result of this, the board seeks to sell the groups operations in Taiwan to repay debt. Highlights uncertainty regarding funding of HSBC after 2025. Got 18£m in convertible loan notes outstanding, maturing within 12 months, 22£m in bank debt and 17£m in cash. Expects 90£m - 100£m in revenue. Mainly asset managers own shares here, some are decreasing their stake, others are increasing it. Specialy situation, pass for me.

303) Ironveld (Ticker: IRON)

6£m unprofitable mining and processing company, producing iron powders, vanadium slag and titanium slag. Just raised 0,9£m. Trading was suspended due to delayed annual results. Pass.

304) Itaconix (Ticker: ITX)

14£m unprofitable company using plant-based polymer technology to enhance sustainability of consumer products (most revenue related to cleaning products e.g. for laundry). Latest results show 30% growth with increased gross margin and reduced losses.

Aiming for ‘mid-term profitability’ by scaling their business. Management is happy with recent results, considers traction of products in the market an ‘important inflection point’. Co-Founders are CEO (owns 8%) and CTO. No long-term debt with 4,2£m in cash. Pass for now, but one to keep in mind.

305) Itim Group (Ticker: ITIM)

17£m provider of software for store-based retailers to optimise their businesses. 70% of revenue is recurring. Latest results show 11% growth driven by non-recurring project services related to implementing their software, which is the segment that ‘drives profitability and cash’. This may explain why last FY was an unprofitable one as project revenues were lower. CEO and founder owns 38%, ‘Lewis family’ owns 18%. Highlights competition with SAP, Microsoft and Oracle. Aiming ‘to differentiate ourselves by focusing on delivering tangible business outcomes for our customers.’ Well, I’m pretty sure that’s what SAP wants to achieve as well.

Wants to focus on growing the project segment, hoping this will result in higher ARR. Receivables growing despite ARR being flat YoY. Capex for intangibles ~10% of revenue. 27x fwd. P/E (Koyfin). Not sure if the focus on implementing software for customers makes sense when the usage of the software by customers over the medium-term is not profitable for ITIM (but maybe that’s a usual dynamic in software, no idea). Pass.

306) ITM Power (Ticker: ITM)

A stock some may remember from the 2021 clean-energy bubble. 472£m designer and manufacturer of electrolysers for production of green hydrogen. Was down ~95% from its peak, stock more than doubled in May on a raised guidance and contract announcements. Generally, there are many announcements for partnerships and supply agreements. Revenue grew 50% to 26£m in FY25, but losses were growing as well. Expects growth to continue while unprofitability persists. Linde holds 16%. Does not seem ITM is near profitability, pass.

307) IXICO (Ticker: IXI)

11£m company for neuroscience imaging and biomarker analytics using AI. Analyses neurological clinical trials. Has been operating profitable in the past, but revenues are down 35% since 2020 and losses grew. Expects to return to growth this year and sees a path for ‘medium-term profitability’. Even if they return to 2020’s profits of ~1£m it’s not extremely cheap, no insider ownership. Pass.

308) Jade Road Investments (Ticker: JADE)

2£m asian investment company without any investments or other revenues since May 2024. Another company bought JADE shares worth 1,2£m through a fundraise. Pass.

309) Jadestone Energy (Ticker: JSE)

98£m unprofitable O&G company operating in Australia, Indonesia, Malaysia and Vietnam. Latest trading update highlights 20% production growth and reduced costs. Sold its Thailand operations to reduce debt. Detailed H1 report on 30 of September. Pass.

310 - 311) James Halstead (Ticker: JHD / JHDA)

660£m manufacturer and distributor of commercial and luxury flooring. Expects FY25 to be a flat year. Slow grower: revenues 8% above levels seen in 2019. New executive Chair (Halstead family) and CFO since last year, CEO joined in 1987 and was promoted to his role last year as well. No long-term debt, >5,5% dividend, fwd. P/E of 16 (Koyfin). ‘James Halstead Settlement’ holds 17%. Stable, boring company, hard to see a meaningful bull case here, pass.

312) Jangada Mining (Ticker: JAN)

5£m no-revenue mining development company with projects in Brazil. New CEO. Pass.

313) Jarvis Securities (Ticker: JIM)

10£m stock broker for retail and institutional clients. CEO owns 41%, three other family members own 4% each. Shares dropped 70% in April as management sold its retail execution-only brokerage business for 11£m and announced to shut down all operations to turn JIM into a cash shell. This process is estimated to take up to 15 months and management seeks cancellation of trading. Announced a 20% special dividend in July, unclear whether there will be more cash returns or the controlling family just keeps it. Pass.

314) Jersey Oil & Gas (Ticker: JOG)

46£m pre-revenue O&G business in the North Sea. Share price moved up, not sure why, but management highlights cost cuts. Pass.

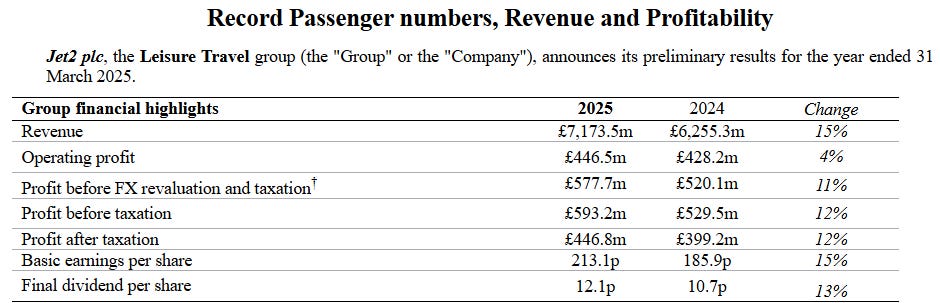

315) Jet2 (Ticker: Jet2)

2,75£b UK-based airline. Launched a 250£m buyback in April after repurchasing nearly all of their convertible bonds for 301£m. Latest numbers looking solid:

Passengers up 12%, new bases on Bournemouth and London airports, 2£b in net cash. Expects ~580£m profit before tax for FY26. 6,5x fwd. P/E (Koyfin). I’m not a fan of airlines and probably never will buy shares of one, but Jet2’s fundamentals are looking really solid for such a capex heavy, cyclical, competitive business:

CEO joined in 2009 and got promoted to CEO in 2020. Philip Meeson, founder of Jet2, retired in 2023 but still owns 15% of shares. Is investing to build up an Airbus 321neo fleet to replace the Boeing 737-800NG. Guides for about ~1£b a year in capex starting 2027. Airlines are a pass for me, but if you are interested in Airlines then I’d say take a closer look here. Write-up by @Matt Newell:

316) Journeo (Ticker: JNEO)

84£m provider of public transport and related infrastructure solutions. I have looked at them before, but can’t remember why I passed. There was some customer concentration, but in FY24 no customer accounted for more than 10% of revenue anymore. 5% insider ownership. Recent update shows flat profits and a slight decrease in revenue due to a delayed project, but sales are just postponed to H2. Orders of 30£m. Aiming for 100£m in revenue (50£m last year) and double digit operating profits (4,8£m last year) in the medium-term.

Just acquired an infrastructure protection system integrator for 10,7£m, which adds 17£m in revenue and 1,4£m in PBT. CEO and Chair joined in 2013. Relying on big infrastructure projects is a key risk here. Fwd. P/E of 18 (Koyfin). Interesting enough for me to take a look again, watchlist.

317) Jubilee Metals Group (Ticker: JLP)

96£m profitable company ‘focused on the treatment of both surface tailings materials and primary mineral ore generated from 3rd party mining operations.’ Latest results show 51% sales growth and EBITDA of 13,6£m for H1. Expanding its copper and chrome operations. Pass for me.

318) Judges Scientific (Ticker: JDG)

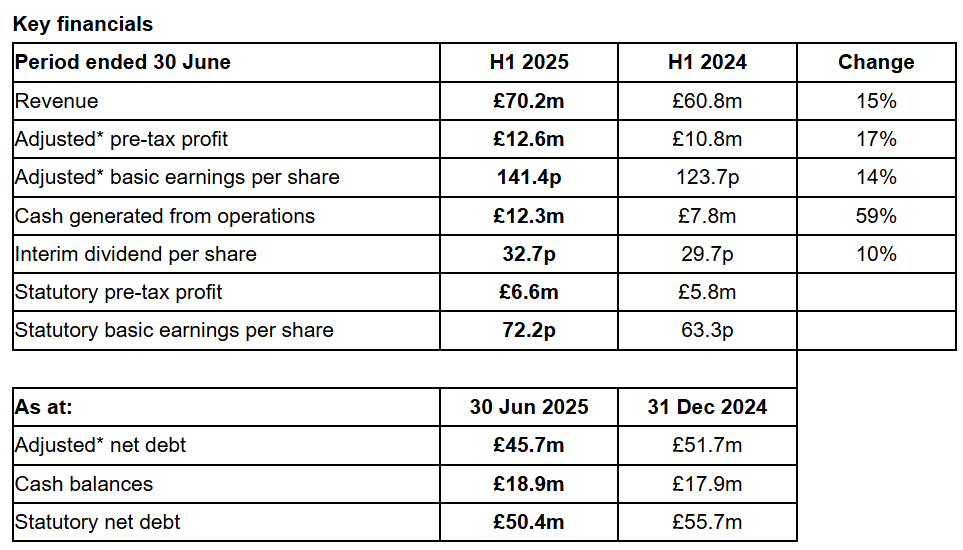

423£m serial acquirer within the scientific instruments sector. A well known company among serial acquirer fans. H1 results looking solid after a more challenging FY24:

Organic revenue up 7%, order intake up 4%. COO will step down in September 2026 after 9 years. CEO is the founder and owns 10% of shares. Weak US market is a headwind currently due to limited research funding. Management is rather focused on restoring organic growth than M&A. Last deal in August 2024, paid 12£m (7x PBT).

Expects adj. EPS of 288p → ~21x adj. P/E for 2026. Adjustment mainly refer to amortisation of acquired intangibles what I consider a fair adjustment. Revenues and profits are H2 weighted. I have JDG on my watchlist since ever and it stays there, 21x adj. P/E on depressed US demand could be interesting, at least if one believes JDG will perform as in the past fundamentally. Great overview by @Compound & Fire:

319) Karelion Diamond Resources (Ticker: KDR)

1£m no-revenue copper & diamond exploration company with projects in Ireland and Finland. Pass.

320) Kazera Global (Ticker: KZG)

15£m African, no-revenue exploration and development company focused on various resources. Pass.

Wrap-up

320/669 companies covered so far.

Watchlist: 45/320.

Pass: 275/320.

No-Revenue counter: 73/320.

Feel free to provide opinions and sources on any of the stocks. Cheers.

Good read. There are several companies worth adding to a watchlist. Of course, there are several basket cases that should be avoided.

I note that three of the companies on the list have previously featured in our coverage. Itaconix was an old favourite — until we raised concerns following the flooding event. If memory serves, the share price more than doubled before that point.

Jet2, as you rightly point out, isn’t just an airline. We exited at 1,560p, locking in a 15% gain, plus dividends — not a bad outcome.

As for Journeo (122p), it has performed remarkably well — in fact, it’s outpaced even our most optimistic expectations. At this stage, I’m genuinely wondering whether we should continue holding or consider banking the gains. There is some profit-taking at the moment, which is to be expected, but it's a solid company with ambitions to double its revenues from current levels. How quickly that happens is open to question. I think it will fulfil its stated objective.

FREE Journeo article if anyone is interested. https://smallcompanychampion.substack.com/p/journeo-plc-55b

Judges Scientific is letting us down at the moment. My son featured the company as a recovery bounce at 10,70. However, while Judges has navigated 2025 with group-level growth, US-specific funding cuts have overshadowed progress, capping the share price upside. Investors are watching H2 for signs of stabilisation. So far, it's by far our worst performer at 6,200p, but there are signs the worst is behind it. Famous last words, and all.

FREE Judges https://open.substack.com/pub/smallcompanychampion/p/judges-scientific-plc?r=kcv2o&utm_campaign=post&utm_medium=web&showWelcomeOnShare=true