SDI Group H1 FY24 Recap

SDI Group H1 FY24 Recap

Shedding light on unexpected weakness

SDI Group (LSE:SDI) surprised investors last thursday as the company cut its FY24 outlook which was provided in a trading update just 2 months ago. If you don’t know the business yet I recommend you to check out

write-up on SDI Group.In September SDI confirmed market expectations for FY24 of £71m in sales and £9,8m adj. PBT. There was no comment on sales but adj. PBT outlook was cut to £7,9m - £8,4m. The main reason, beside an overall slowdown in China and Germany, is some destocking of a major customer of Atik Cameras, a subsidiary of SDI. This customer reorganized its procurement and decided to order less than anticipated after SDI confirmed expectations.

We thought we could have a good shipping going out the door [...] but sadly, it didn't. [...] It was just last minute.- Mike Creedon, CEO SDI Group.

So the unfortunate communication, which seems like a little clown show at first, is because of unlucky timing.

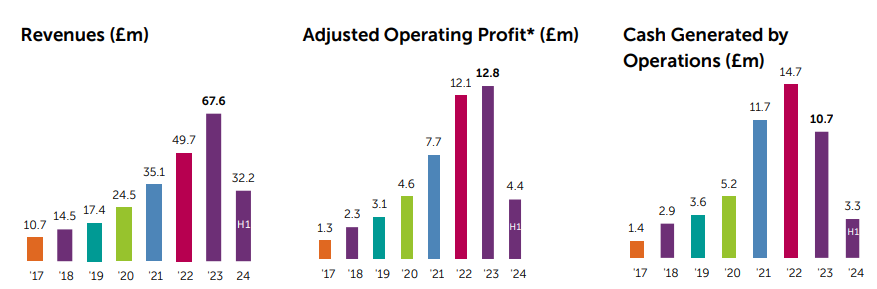

The numbers

Quick reminder: SDI benefited from Covid due to some large test contracts that expired at the end of FY23. Therefore, H1 2023 numbers include these one-off sales unless otherwise stated.

Revenues increased by 1,6% to £32,2m

Organic growth came in at 2,2% excl. COVID sales whereas the S&C division showed solid 6,7% organic growth, while digital imaging declined double digits mainly due to mentioned destocking.

EBIT dropped by 39,2% to £3,4m, implying a 10,5% margin, down from 16,7%, as anticipated. This once more confirms that the COVID sales were high margin.

Due to higher financing costs PBT, declined 50% to £2,65m

Free cash flow came in at £1,7m, which is an improvement compared to H1 2023, but nevertheless was impacted by £2.7m reduction in customer advances.

In FY23 we saw a inventory build up of roughly £3m which is now partly reversed. Management said working capital improvements will be a key point for H2, so we can expect some freed up cash.

Bank debt was reduced by £1,25m.

M&A

There was no M&A activity in H1, however SDI acquired Peak Sensors Ltd in November for a total consideration of £2,4m net of cash funded with debt. Peak sensors had £2,1m in sales and £0,33m in EBIT last FY which puts a 1,1x sales and 7,3x EBIT multiple on this acquisition.

Peak Sensors is a leading UK manufacturer of temperature sensors, specialising in standard and bespoke thermocouples and resistance thermometers. - acquisition announcement

During H1 £1,0m in contingent consideration were paid for the acquisition of SVS in 2022. This payment depended on adj. EBIT to be above > £1,1m for latest FY. For context, SVS was acquired with an EBIT of £0,7m.

SVS is proving to be a 'lumpy' order (and revenues) business. As a result of the events in Ukraine, its major OEM customer has had to re-schedule it's planned order profile, leading to a delay in placement of its next order for its next sputtering machine. Their pipeline remains strong but timing of order placement can be variable. - interim results

Management said their acquisition pipeline is strong. Referring to the FY23 call in August, where Mike Creedon was confident to do 2-3 acquisitions, it is likely we see at least one more for FY24. But they also highlightend they will not do any M&A deal just to hit a certain number of deals for a year, so I would not bet my money on that.

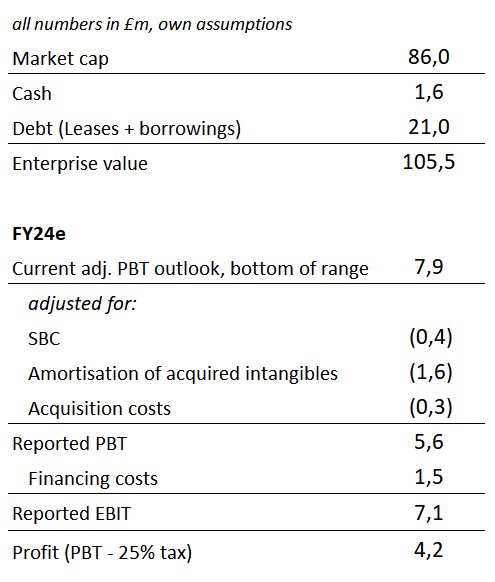

Valuation

Based on these FY24e assumptions above we get a ~15x EV/EBIT or ~20x P/E multiple. Regarding free cash flow (before M&A) we can expect some working capital improvements in H2, so asuming there is no wc impact for FY24 we can expect ~£7m - £8m FCF or a 6,7% to 7,5% FCF yield.

These valuation levels are far from a screaming buy. However, if you believe we are observing somewhat depressed earnings due to destocking and are confident in seeing mid-single-digit organic growth combined with favorable M&A deals going forward, these levels may be interesting to build a position. Nevertheless it doesn’t need to be mentioned that these priced levels were way more attractive some weeks ago.

Things good to know

SDI is currently implementing a new financial consolidation system which should provide more scalability as more businesses are added

Currently the group consist of two operating segments: digital imaging and sensors & control. Work is in progress to restructure the segments into lab products and industrial/scientifc products to provide more accurate information.

In 2022 there were three M&A deals where real estate was included with a value of £4,6m. The board is currently discussing sale-lease-backs for these properties.

If you follow SDI you know, low insider ownership is alway a discussion point. Things haven’t change that much but there were some buys in November and December by Mike Creedon and other insiders.

Current insider holdings

All in all SDI is kind of a wait and see story for now. I feel like after COVID impacted this company, some dust has to settle in FY24.

I hope I could provide a good overview over their H1 earnings and will continue to write earnings recaps for SDI.

Cheers.

Hi, thanks for the feedback.

Something that bugs me (but most likely due to poor understanding on my side) is that organic growth at 2.2% is large than revenue growth of 1.6%. I do get how to explain that.