Welcome to part 9 of my A-Z on AIM.

Only 15 tickers today, personal live is eating up a lot of time currently. In this one you’ll find many marketing businesses next to an interesting niche bank, professional services, PE and as always: at least one pre-revenue energy/mining company. 9 out of 15 are profitable. Let’s go!

Here you find the other parts: https://increasingodds.substack.com/s/a-z-uk-aim

166) Dianomi (Ticker: DNM)

8£m provider of digital advertising services for business and finance content. Latest results show -7% revenue, but with increased gross margin and reduced costs, profitability was reached: 0,2£m operating profit for FY24. No long-term liabilities and whole market cap in cash.

The overall traffic on its ads increased by 4%, but spending among advertisers was down 4%. Works with 341 publisher, +1 in 2024. CNN seems to be their biggest customer. New partnership with Microsofts ad platform. 10% insider ownership, both co-founders are on the board.

Expects reduced profitability due to increased investment in sales people and lower gross margin as their revenue share in new publisher agreements is lower than usually. Rather a pass for me, the blue chip customer base in its niche is interesting, but bumpy profits in the competitive ads market suggests this niche expertise is not as valuable.

167) Digitalbox (Ticker: DBOX)

5£m operator of websites for entertainment news, e.g. satirical content and celebrity news. Generates revenue through advertising and subscriptions. CEO wants to double the size of the business in the next 3 years. Just acquired The Life Network for 0,2£m, the assets will be used to develop the Royal Insider, a website focussed on news about the Royals. Operates unprofitable, 6,3£m impairment last year. Definitely a pass for me considering the type of content they create.

168) Dillistone Group (Ticker: DSG)

2£m provider of software and services that enable recruitment firms and in-house recruiters to better manage their selection process and address the training needs of individuals. Mostly recurring revenues, but down 12%. Profits increased through cost reductions and restructuring in 2023. But operates on the edge of profitability. Recent AGM update highlights new customer wins, if H2 looks similar, FY25 will definitely be better than FY24.

The wife of the CEO provided a 120£k loan with an 11% interest. Also raised some cash to pay down debt. Somehow there is zero cash and zero cash equivalents on the sheet. Pass.

169) Directa Plus (Ticker: DCTA)

20£m producer of pristine graphene nanoplatelets, used in environmental remediation and textile industry, with its own patented production process. Revenues down 40% due to order delays, growing losses. Order book is about 1x annual revenue. Founder is CEO, owns 4%. 40% is owned by Nant Capital. Pass.

170) Distil (Ticker: DIS)

3£m owner of drinks brands Blackwoods Gin and Vodka, RedLeg Spiced Rum and Blavod Black Vodka. Appointed Robert Grain as CEO who owns 26% of shares through its company. Don’t know if he has any expertise, DIS describes him as a whiskey enthusiast. Operates highly unprofitable and revenues are bumpy. Announced a distribution partnership in the US. Pass.

171) Distribution Finance Capital Holdings (Ticker: DFCH)

65£m specialist bank providing working capital solutions to dealers and manufacturers. FY24 numbers look really strong: New loan originations up 20% to 1,4£b, closing loan book up 15% to 666£m, interest up to 7,9%, profit up 4x to 19£m. 2,5% of dealers in arrears or 0,6% of loans. Q1 update confirms this development.

Wants to double its loan book, increase ROE to mid teens and maintain high interest rates. Expects loan book to close at 750£m to 800£m for 2025. Various wealth management firms in top 10 shareholders, no insider ownership. Banks are usually not my cup of tea, but this niche focus somehow makes me interested. Launched a buyback programme for 10% of shares or 5£m. Watchlist.

172) Dotdigital Group (Ticker: DOTD)

229£m provider of cross-channel marketing automation technology to marketing professionals. Appointed new CFO. 95% recurring revenue. Latest results:

Consitenly growing but profit margin decreasing over the long-term, from >20% in 2014 to <15% now. 15x fwd. P/E. Confident to keep growing in 2025. Small dividend. Co Founder & President owns 10%. No debt. Not sure whether they depend on money spend on ads or if its rather a platform for CRM, but considering valuation, stable growth, clean balance sheet, co-founder involved, this one is fairly interesting. Watchlist.

173) DP Poland (Ticker: DPP)

90£m operator of Domino’s Pizzas stores in Poland and Croatia. Just acquired Pizzeria 105 for 8,5£m (9x EBITDA) to add 90 stores to its system. The seller agreed to reinvest one third of the proceed into DPP through new shares. DPP delayed its annual results, so we don’t have exact numbers for 2024 yet. Q1 trading update shows 6,5% sales growth, excl. the acquisition, with 3% like-for-like growth. Operates unprofitable.

CEO worked for Domino’s before, Chair was CEO of Domino’s in the UK. So there is a lot of expertise and in the long-run this may be a great story, assuming their expertise turns into valuable growth, but I stay away from unprofitability without a path towards profitability. Pass.

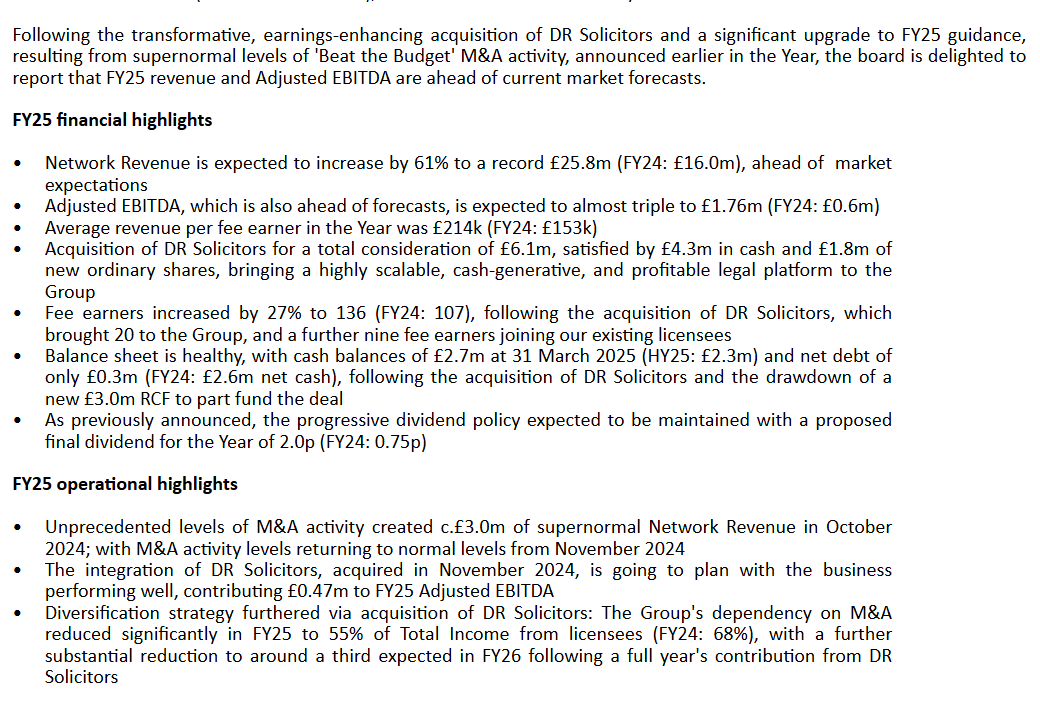

174) DSW Capital (Ticker: DSW)

14£m professional financial services network. New CEO in line with succession plans.

We recruit highly skilled professionals (typically “Big 4”) in focussed niches of expertise to run their own business and provide services to small to mid market corporates and their owner managers

Co-Founders are still involved. DOW stands for Dow Schofield Watts, the Dow’s own 16,5%, the Watts own 12%, the Schofields own 5%. 9x fwd. P/E. Financials seem a bit bumpy despite a capital light business model. No debt.

For the germans, here is a podcast about DSW by @Christian Schmidt . I’ve read about DSW many times over the last years but never thought it’s one for me, pass.

175) Duke Capital (Ticker: DUKE)

148£m provider of hybrid capital solutions for SME business. Hybrid refers to a mix of private equity and credit. Currently 234£m invested. Directors own 4%.

No venture capital, but seeks exits as companies grow. Founders are still involved. Operates highly profitable, but margins are bumpy due to accounting impacts of exits. I prefer investing in serial acquirers if I want the SME exposure instead of these more aggressive PE players, personal preference. Shares outstanding doubled since 2019, 8% dividend, not sure if it’s sustainable or a one-off. Pass for me.

176) Eagle Eye Solutions (Ticker: EYE)

63£m SaaS company for personalized marketing, seems focused on services like loyality programms. Founder just stepped down from his CIO role. The other co-founder is CTO. 80% recurring revenue. Shares down 55% Ytd after a flat H1 and loss of a 10£m high margin contract. 6% profit margin in H1, so this loss likely results in a lower margin or even unprofitability, which we saw in H1 2024 anyways. Aims to double its revenue with increased margin until FY27. Sentiment seems really bad right now. Assuming they reach 100£m revenue on 30% adj. EBITDA margin (which maybe leads to 10-12% profit margin) it’s cheap. Questionable if it’s a realistic goal considering the contract loss and flat H1. Pass.

177) Earnz (Ticker: EARN)

5£m energy service company created from a cash shell. A lot of director dealings and share placings. Acquired multiple businesses. At least one where I find some numbers is operating profitable, but profits are shrinking on growing revenues. No M&A track record makes setups like this uninteresting, pass.

178) Ebiquity (Ticker: EBQ)

32£m market cap. ‘world leader in media investment analysis’, whatever that means, but it seems to be about helping businesses to make better marketing decisions. 2024 numbers look ugly due to market environment.

Don’t want to spend more time here. The advertising market is cyclical by nature and business models like this, with a high cost base, suffer from a downswing like asset heavy industrial companies. Pass.

179) Eco Atlantic Oil & Gas (Ticker: ECO)

I hoped for the first part without energy or mining companies …

31£m no revenue O&G exploration and development company with projects in Guyana, Namibia, and South Africa. Just received exploration rights by South African government. Pass.

180) Eco Animal Health (Ticker: EAH)

42£m developer of veterinary pharmaceuticals, focussed on pigs and poultry. Recent trading update suggests higher than expected profitability (>7,2£m adj. EBITDA) due to increased gross margin and cost control. Considers improvements sustainable, but does not update FY26 and FY27 targets as revenue for the full year will be 7% below market expectations (85,3£m). Profits seem to be H2 weighted.

New Chair in line with succession plans. During this series we came across some other livestock businesses, I avoided all due to exposure to commodity-like markets. EAH highlights cyclical markets too, currency headwinds (China exposure) and demand is dependent on development of deseases. 34x fwd. P/E. Provides outlook up to 2035 based on R&D pipeline. Maybe that’s a common thing in pharma but rather seems like entertainment to me. Pass.

Wrap-up

180/669 companies covered so far.

Watchlist: 29/180.

Pass: 151/180.

No-Revenue counter: 38/180.

Feel free to provide opinions and sources on any of the stocks. Cheers.

Good stiff Saesch. There really is a lot of dross you have to wade through on AIM