Exploring AIM: A-Z Part 12

Deep Value NAV > Market Cap and Quality High-Growth

Welcome to part 12,

quality is finally improving and I came across the small niche companies this series is looking for. Small companies with cash close to market cap, Falkland Islands service company, serving the 3600 people living there next to the one million penguins and some actually solid high-growth companies. One of the more interesting parts for sure, 3 for my watchlist. Let’s go!

Here you find the other parts: https://increasingodds.substack.com/s/a-z-uk-aim

211) Fadel Partners (Ticker: FADL)

13£m developer of cloud-based brand compliance, rights and royalty management software used by marketers, finance teams and licensers. Recent trading update:

Most revenues recurring and cost reduction ongoing. Board expects revenue for FY25 to be 12-13£m. CFO will step down in September. CEO is the founder who owns 20%, his brother owns 10%, brother in-law owns another 4%. Far from profitability, pass.

212) Falcon Oil & Gas (Ticker: FOG)

85£m no-revenue O&G exploration and development company with interests in fields in Australia, Hungary and South Africa. There are some positive drilling results in recent RNS announcements. Pass.

213) Faron Pharmaceuticals (Ticker: FARN)

244£m no-revenue clinical stage biopharmaceutical company from Finland with a pipeline based on the receptors involved in regulation of immune response in oncology and organ damage. Recent RNS statements seem to be positive. No noteworthy insider ownership. Pass.

214) Feedback (Ticker: FDBK)

6£m software provider for healthcare workflows. About 1£m in revenues on 2£m losses. Highlights delays of projects due to cost savings by UK’s national health service. Raised 6£m in Nov 2024, therefore it’s well funded. No meaningful insider ownership. CEO joined in 2019. Pass.

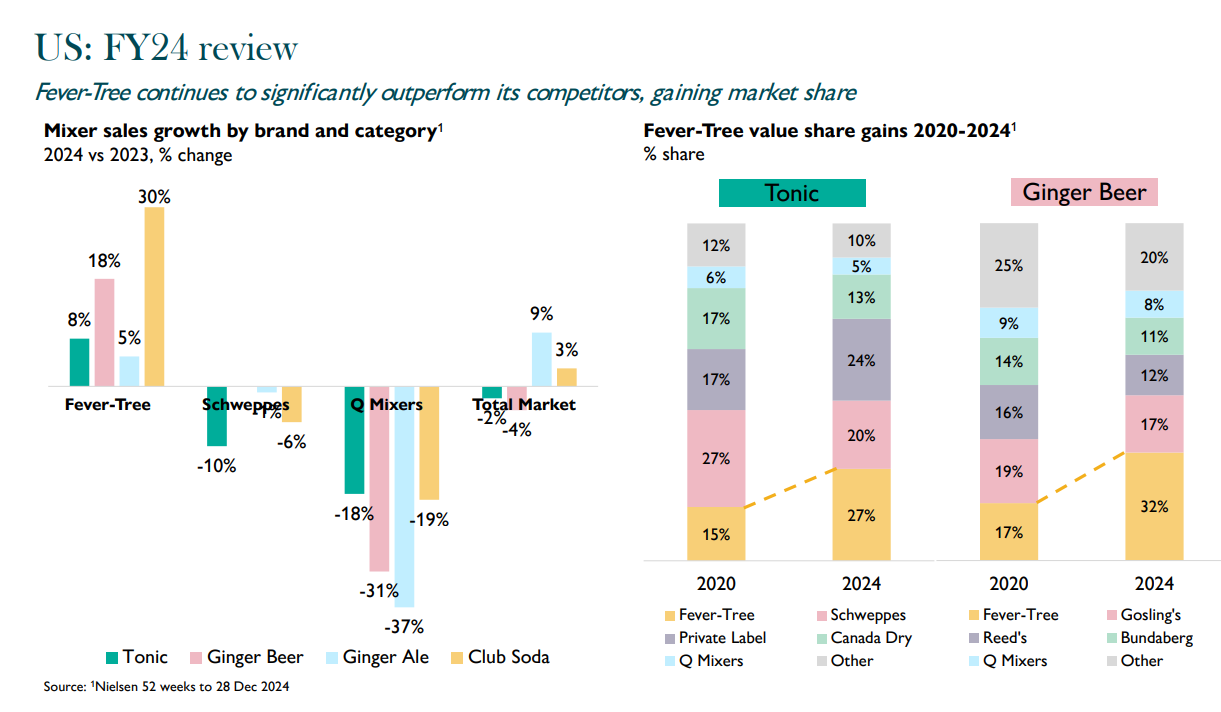

215) Fevertree Drinks (Ticker: FEVR)

1126£m supplier of carbonated mixers such as tonic wasters, sodas, gingers, lemonades and more. Expects low single digit revenue growth for FY25 and 12% adj. EBITDA margin. Highlights successful partnership with Molson Coors in the US. 10% tariff will be splitted between both companies, but FEVR wants to increase production based in the US anyways. Molson Coors owns 8,5% of shares. 100£m share buyback ongoing (71£m + a 29£m extension), financed from the Molson Coors deal as it seems. 6% insider ownership. CEO and CFO joined in 2014.

Saw a hit on gross margin through higher glass and freight costs. GM did recover and freight costs should be reduced in the medium-term due to the US onshoring. US accounts for about 35% of revenue, expects double digit growth through the partnership and considers the US to be the growth driver for the whole group as market share is growing rapdily, even prior to the partnership:

In Europe, market share is slightly growing. Main competitor is Schweppes. Interesting story overall, but the price already catched up on it. Fwd. P/E doubled to 40 since the partnership was announced. I would not give them credits for the buyback as it only reverses the share issue of Molson Coors' investment. There have been no buybacks under the current CEO/CFO before. Pass. Nevertheless I want to highlight @

, who pitched FEVR after the announcement and well, he got it right, great post:

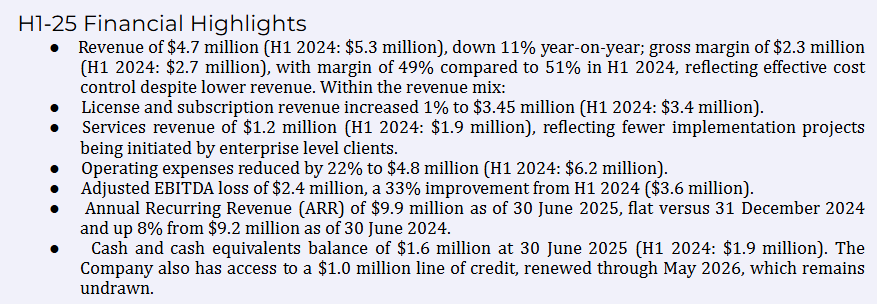

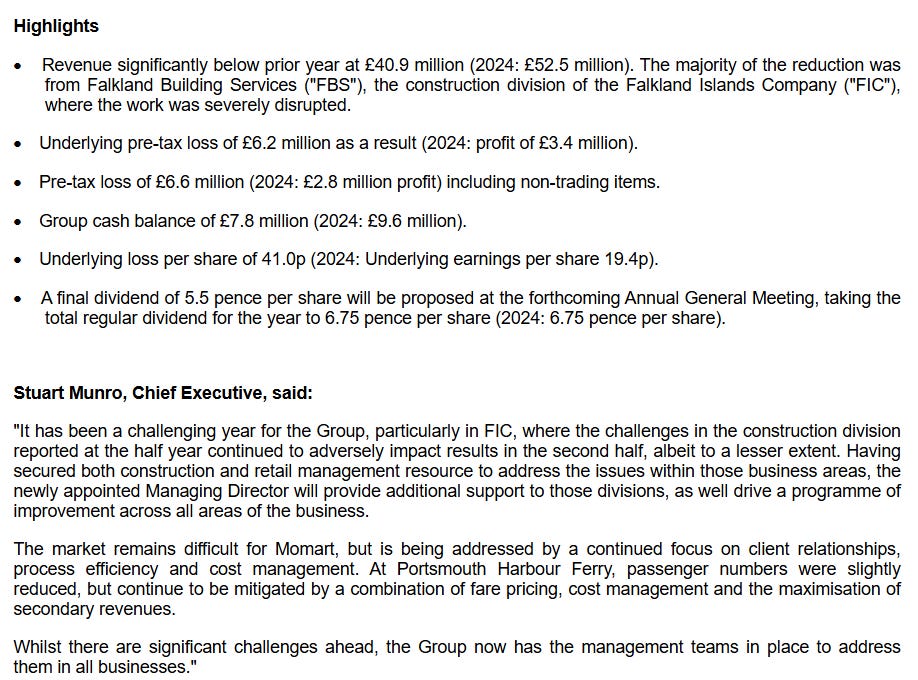

216) FIH Group (Ticker: FIH)

26£m group offering various services such as a ferry service in Portsmouth, art logistics and storage or construction and retail services on Falkland Islands. FY25 was a tough year due to the construction sector:

Looking at the last 5 years, 2020-2022 were flat, while 2023 saw a big jump in revenue (probably M&A?). 2024 was flat again and 2025 has been a down year. Looking as the services it seems like some are very unique with high barriers to entry (e.g. ferry service) while others are unique due to their focus on the Falkland Islands. At the same time this focus limits growth possibilities. That’s why management is looking for acquisitions. The focus comes with risk as it seems, their construction division did zero revenue in 2025 (down from 11£m in 2024) because one big project was delayed. Pass.

217) Fiinu (Ticker: BANK)

35£m no-revenue fintech offering ‘unbundled overdraft solution without anyone needing to switch banks. Fiinu will become the first Open Banking led interest income/deposit margin banking infrastructure provider. The bank-agnostic fintech platform will be serving all other UK bank customers, of which circa 55-60% do not have access to arranged overdrafts. The group intends to licence its technology platform, especially in the markets where it does not want to set up banking operations’.

As you can see in this description, it’s very early stage. Share price 15x as they announced their first deal with a UK Bank in Jan this year. Some share issues, wants to acquire Everfex P.S.A, a FX brokerage service. Pass.

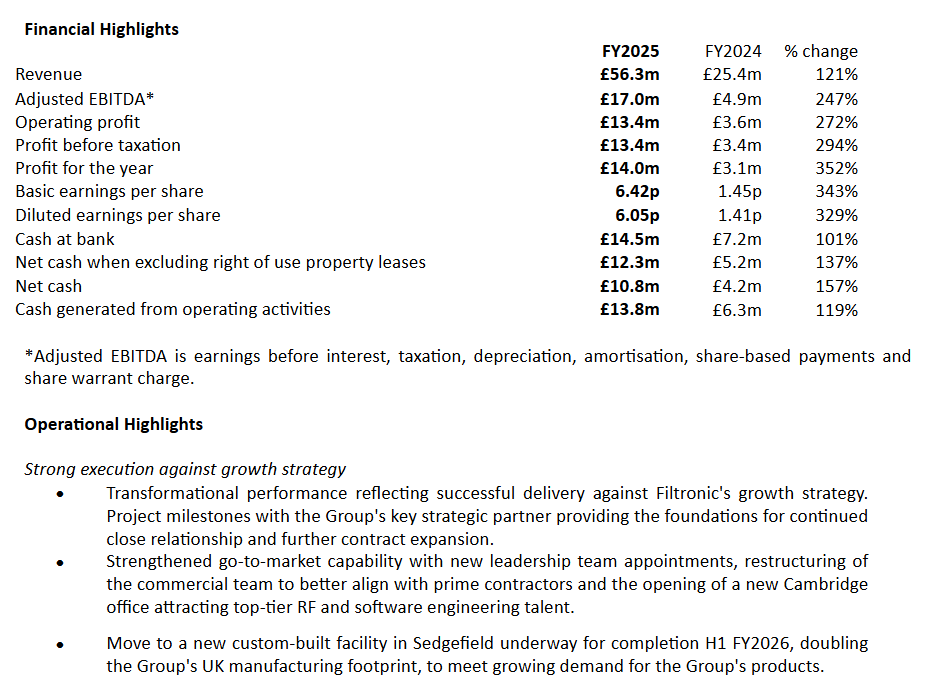

218) Filtronic (Ticker: FTC)

307£m global telecommunications, space, aerospace, and defense company providing design and manufacturing of high-frequency communication solutions. Share price 10x in last 2 years. Seems like a solid, high-growth company:

Agreements with SpaceX, Airbus and ESA. Also working with Leonardo and BAE. Space is 80% of revenue, also seems to benefit from increased European defense spending. Is confident to deliver great performance in FY26. No insider ownership. Seems to be one of the rare solid high-growth companies on AIM. Fwd. EV/EBIT 40 (Koyfin). Not my cup of tea, but likely interesting for others.

Those who follow me for some time know that I often mention Koyfin. This is not sponsored and there is no ref-link or anything, I just want to use my little reach to recommend a good tool I’m using since over two years now (Free version, mostly the watchlist and graphs features). @

just gave an update on the recent development:

219) Finseta (Ticker: FIN)

14£m foreign exchange and payments solutions company offering multi-currency accounts to businesses and individuals. Recent trading update shows 16% revenue growth driven by more customers. Corporate customers account for 58% of revenue. Expects a stronger H2 with increased margins. Group is operating profitable, margins are a little bumbpy due to growth investments.

Chief Commercial Officer owns 16%, CIO owns 4%. There are some other >5% shareholders who are neither on the board or part of the C-suite. The growth story seems to be intact.

I have FIN on my watchlist since @

pitched it in March last year, FIN was formerly known as Cornerstone FS:

There is a lot to like about payment businesses generally. It’s usually strongly regulated, so if you find your spot in this market you can likely build on that for some time. Total addressable market is huge even in niches within the payments world and business models are usually scalable. Nevertheless, it’s a complex market with a lot of players, so it’s kinda part of the ‘too hard’ pile for me, but at some point I’ll spend more time with payment businesses. Watchlist.

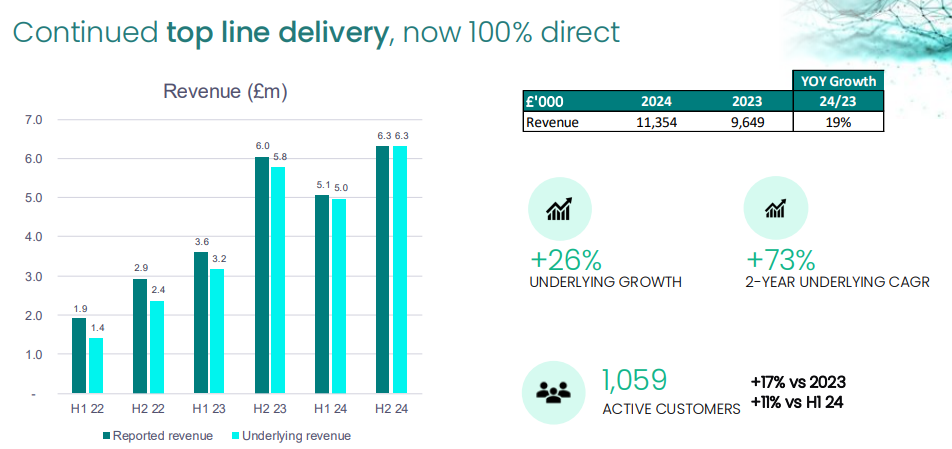

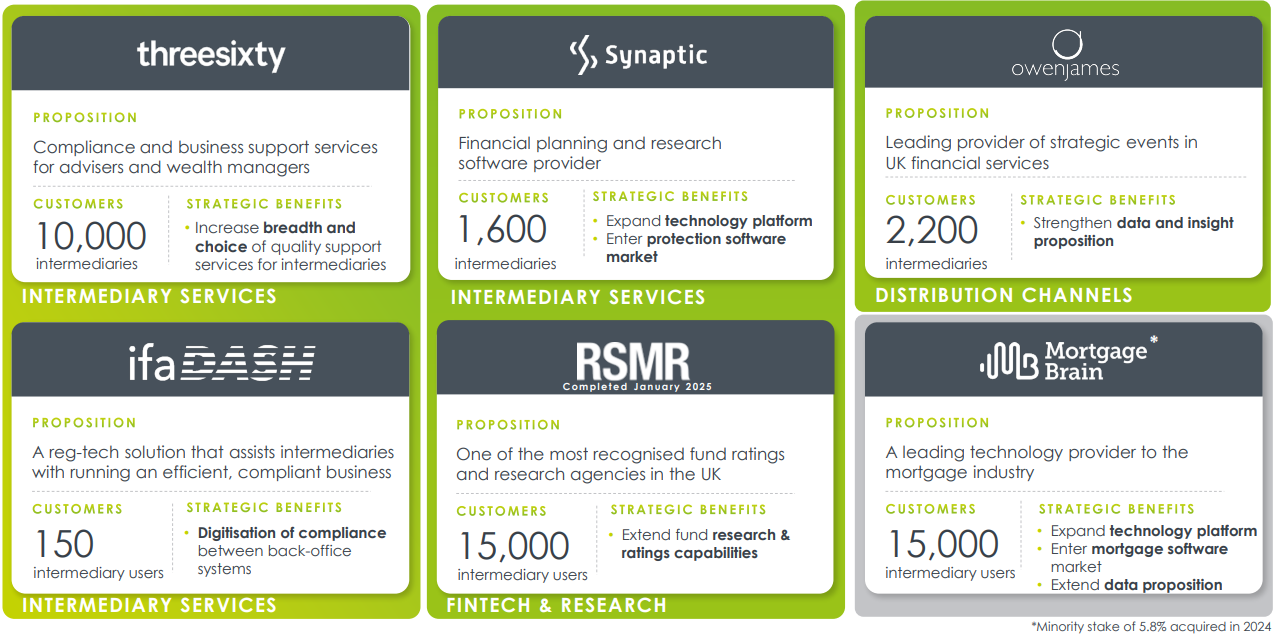

220) Fintel (Ticker: FNTL)

232£m provider of compliance and regulatory support for intermediary businesses such as wealth managers or mortgage brokers and distribution services for banks or pension companies. Recent TU shows 18% revenue growth, mostly inorganic. 57% of revenues is recurring. Founder owns 24% and is non-executive director. CEO joined in the founding year 2002 and joined the board in 2010, owns 4%.

5-7% growth, with mostly recurring revenues and an ongoing M&A strategy definitely seems interesting when considering the expertise of management, the importance of compliance and regulation for their customers and the fwd. P/E of 16 (Koyfin).

About 2/3 of assets is goodwill. Net debt of 32£m. Definitely worth a look at how acquisitions performed in the past. I’m interested, watchlist.

221) Firering Strategic Minerals (Ticker: FRG)

Nothing about this is fire. 6£m no-revenue minerals exploration and development company with projects in Zambia and Côte d'Ivoire. JV partner withdrawed from Lithium Projects. Just raised 1£m. Pass.

222) First Development Resources (Ticker: FDR)

A recent IPO. 7£m no-revenue exploration and development company with projects in Australia. Focused on lithium, rare earth elements, uranium and gold. Power Metal Resources, another listed mining player, holds 43%. Pass.

223) First Property Group (Ticker: FPO)

23£m property fund manager and investor with operations in the United Kingdom and Central Europe with a focus on high yield commercial property. Earns money through fund management and direct investments in properties. Manages eleven funds and directly holds six properties in Poland and Romania. Assets under management of 220£m, down from 274£m. Reduced net debt by 3,4£m (15%) and initiated a cost saving programme. NAV attributable to FPO at book value of 45£m, net debt of 20£m.

Share of associates seems to be the managed fund income while revenues refelect the rental income of owned properties. NAV per share is flat since 2017, but I can’t tell if there have been any property sells. CEO owns 17%, Chair owns 10%. Seems a little complicated to dig through the reports, pass.

224) Fiske (Ticker: FKE)

8£m investment and wealth management firm. Very illiquid. 40% of shares are owned by the Harrison Family, CEO is also part of that. He is with the company since 1996 and CEO since 2014. Fiske owns shares of Euroclear, a financial market infrastructure company, that paid 497£k to FKE last year in dividends. That’s 6% of FKE’s market cap, pre-tax.

Latest trading update from Feb shows 12% growth with increased profits:

What’s more interesting is that FKE is debt free and had 6£m in cash at the end of 2024. New dividends from Euroclear and interest on cash should bring the cash balance towards 6,5£m. Their Euroclear stake is worth about 6£m too. So as you can see, it’s extremely cheap. FKE operated unprofitable in 6 out of the last 10 years tho. Pays a dividend, did some M&A in the past, sold some shares in Euroclear, so it’s not necessarily a sleepy company with a big cash pile. Here I want to highlight the work by @

, who wrote about FKE in more detail and considers it to be too cheap:

FKE is definitely one for the watchlist, but I can’t even buy it from Germany (also not via Interactive Brokers). So for the statistics, it’s a watchlist stock, but in reality, it’s a pass for me.

225) Fletcher King (Ticker: FLK)

4£m advisor for property fund management, property asset management, investment broking, valuations, rating and development. FY25 was flat in terms of revenues while employee expenses grew, leading to decreased profits. No long-term debt and 4,2£m in cash. Outlook:

With the current uncertainty both domestically and internationally it is difficult to see the capital markets improving very much. Having said that, we must be somewhere near the bottom and the market will move forward but when?

Definitely a refreshing non-bla-bla way of saying ‘we have no idea what will happen’. Pays a 6% dividend, trades on 15x P/E. Maybe 10x fwd. assuming recovering property markets. Founder is non-executive Chair and owns 6,5% of shares. 30% is owned CM Strategic 613 Limited. But it does not seem like anyone cares about cash > market cap in that case. They even highlight the solid cash pile on their homepage. Pass.

Wrap-up

225/669 companies covered so far.

Watchlist: 33/225.

Pass: 192/225.

No-Revenue counter: 52/225.

Feel free to provide opinions and sources on any of the stocks. Cheers.

Some great work here, I think you are right that only about 10-15% or Aim interesting, but some of those stocks are v interesting

Fevertree is one I haven't heard about in a while