Exploring AIM: A-Z Part 10

Special Situations: Cash Offers, suspended Operations, suspended Trading.

Welcome to part 10,

after a little break this series is now back to its weekly schedule. In this part we’ll reach ticker number 200 and you’ll be reminded what AIM is all about: quality. Just kidding, only 5/20 are profitable, one of them will be acquired and another saw its operations suspended by the government. Matching that, you’ll find a special situation PE player. Only one for my watchlist, but likely some interesting names for others. Let’s go!

Here you find the other parts: https://increasingodds.substack.com/s/a-z-uk-aim

181) Eco Buildings Group (Ticker: ECOB)

4£m provider of glass fibre and marble products for housing. Marble is quarried in eastern Europe. Just announced a joint venture in Senegal for a new production facility. 2£m in impairments and inventory write-offs last year. Revenues grew strongly but losses persist. Three share issues in the last 16 months for >50% the current market cap. Founder is the executive chair man. Ongoing litigation against the Republic of Kosovo. Pass.

182) ECR Minerals (Ticker: ECR)

4£m no-revenue gold exploration and development company from Australia. Highlights positive test drilling results. Pass.

183) Eden Research (Ticker: EDEN)

18£m biotech focussed on biopesticides for sustainable agriculture. I can’t access the website for some reason, but it’s operating highly unprofitable but growing consistently. Announced a research partnership with Royal Holloway, University of London. Pass.

184) eEnergy (Ticker: EAAS)

15£m project manager for decarbonization projects. Consulting and financing solutions. Gross margin up strongly, revenue up 67% in H1. Aims to be cashflow positive for 2025. Focussed on education and healthcare markets, mostly lighting and solar solutions. Just launched a solar maintenance service. Successful cost control and gross margin increase in combination with a solid project pipeline sparks my interest. Watchlist, but it’s not a high priority.

185) EKF Diagnostics (Ticker: EKF)

139£m diagnostics business focussed on Hematology and Diabetes, also manufactures enzymes and other custom products for use in diagnostic, food and industrial applications. 1£m buyback launched in May. Debt free. Expects revenue of 53,6£m and 12,4£m in adj. EBITDA for 2025. Aims for 80£m revenue and 20£m EBITDA in 2029. H1 2025 was flat, after -5% revenues in 2024, while gross margin grew and costs were reduced. 20x fwd. P/E (Koyfin). Assuming a similar adj. EBITDA to profit conversion rate for 2029, it’s a <14x P/E2029. Probably not a bad business, but that’s it. Pass.

186) Eleco (Ticker: ELCO)

145£m software provider for building lifecycle management, niche computer-aided design and engineering. Recent trading update shows 20% growth, debt free, profitable. 80% of revenue is recurring. Grew 30% since 2020, partly through M&A. CEO joined 7 years ago, held COO role for 3 years. Margins are bumpy around 10%, but they switched from licensing to a recurring model, so margins should be more stable going forward. Trades on 29x fwd. P/E according to Koyfin. Revenue mostly from Europe. This one generally appears to be an average solid software business on a typical valuation level. Pass.

187) Electric Guitar (Ticker: ELEG)

2£m cash shell, suspended from trading as they didn’t find anything to acquire. Pass.

188) Emmerson (Ticker: EML)

24£m no-revenue developer of a potash (used as fertiliser) development project in Northern Morocco. Pass.

189) Empire Metals (Ticker: EEE)

199£m no-revenue titanium exploration and development company from Australia. Share price just tripled and investor from Malaysia doubled its position. Found its titanium to be high quality and the development is progressing. Also announced to expands its team. Pass for me, maybe worth a look for mining people.

190) Empresaria Group (Ticker: EMR)

23£m staffing group which just received a non-binding indicative proposal regarding a possible cash offer by Legacy UK Holdings for 62p per share (current price: 46p).

Noting the previously announced views of the Company's two largest shareholders who have encouraged the Board to explore options to realise value […] The Board is of the belief that the Possible Offer represents the highest value currently on offer to shareholders. Accordingly, the Board has confirmed to Legacy that the Possible Offer is at a price level at which it is minded to unanimously recommend that shareholders accept … [the offer].

The two largest shareholders own 45% of shares. The group was unprofitable in 2024 and got 15£m in net debt. There is a 35% gap to the offer price, so this one may be interesting for merger arbitrage people, but not my cup of tea, pass.

191) Empyrean Energy (Ticker: EME)

6£m no-revenue O&G exploration and development company with projects in Indonesia, Australia and the USA. Just signed a gas sale agreement until 2037 with a government-owned electric power distributor from Indonesia for a gas field where EME owns 8,5%. Pass.

192) EMV Capital (Ticker: EMVC)

16£m venture capital group focused on ‘deep tech’ and life sciences, formerly knows as NetScientific.

Revenue is growing strongly but so are losses, which is expected in early-stage VC. Founder is CEO (owns 14%), Chairman got a life science background. States fair value is of the portfolio is 37,7£m. Pass.

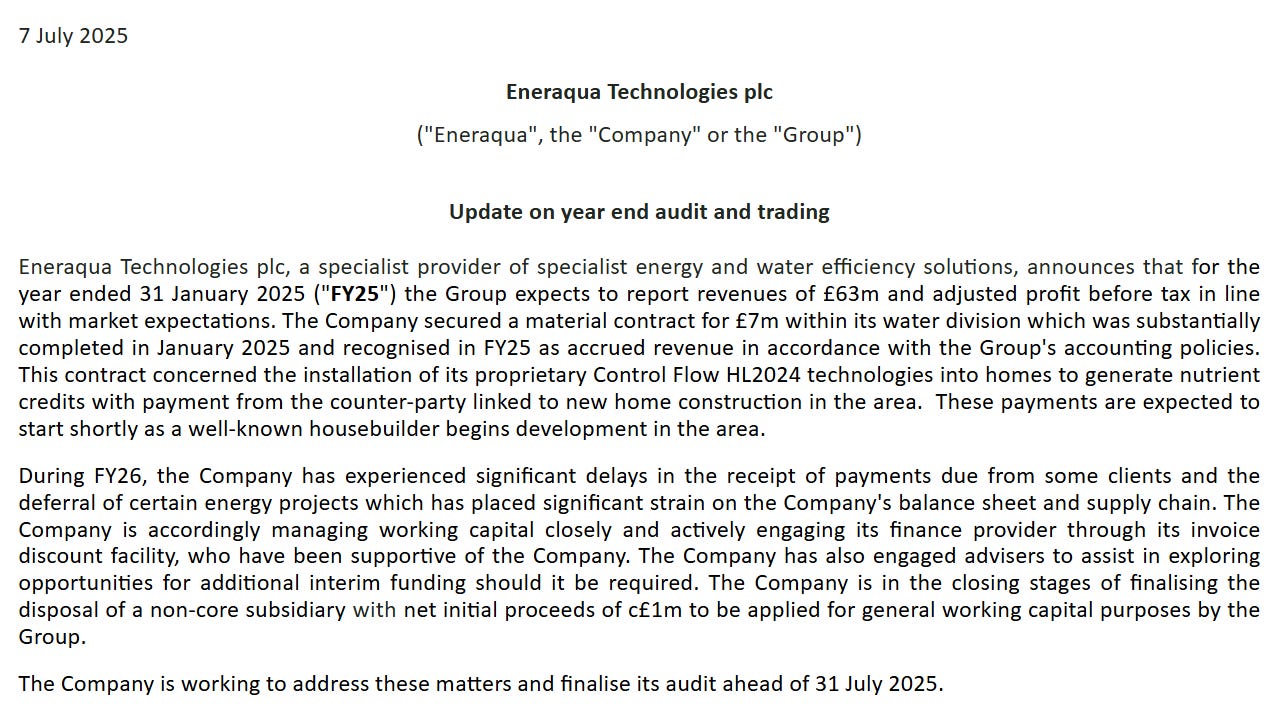

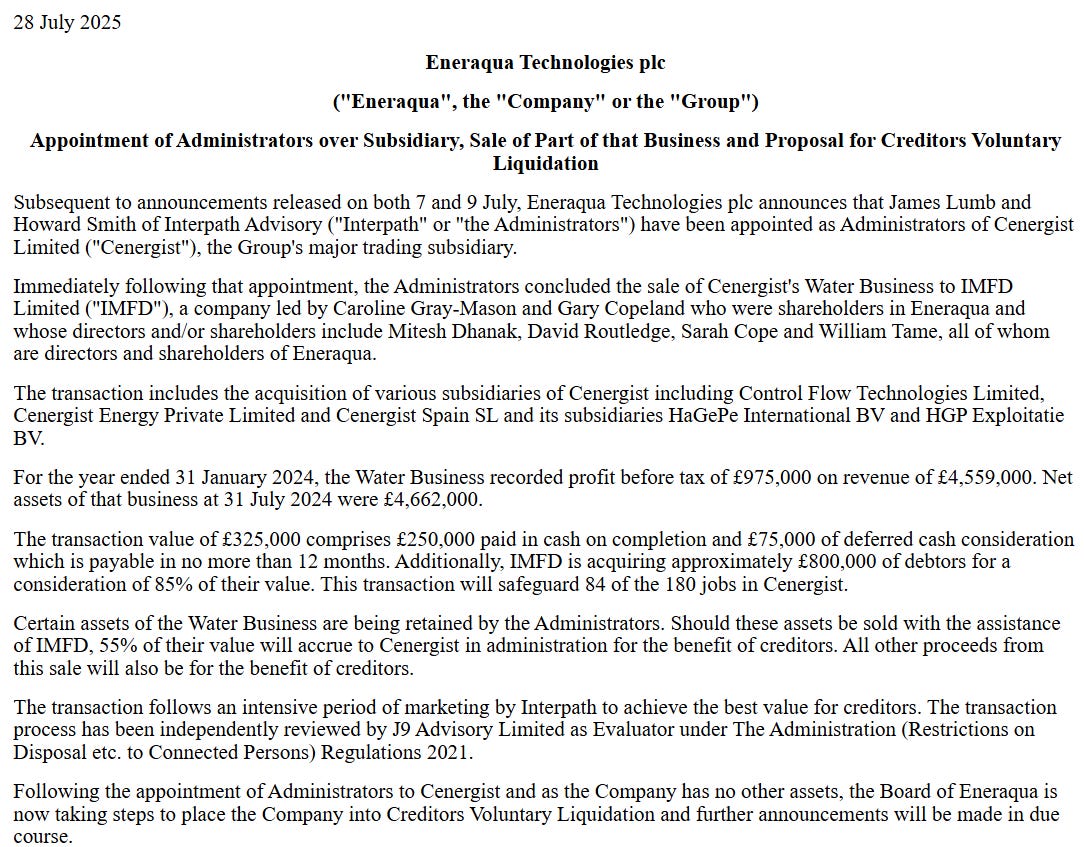

193) Eneraqua Technologies (Ticker: ETP)

6£m specialist in energy and water efficiency providing turnkey solutions for decarbonisation through heating and hot water systems. Suspended from trading due to financial problems.

Selling off assets:

The company produced 8,5£m in profits in 2023, even paid a small dividend. Maybe it’s worth to keep an eye on for those interested in special situations. Pass.

194) EnergyPathways (Ticker: EPP)

9£m no-revenue energy transition company with an energy storage facility project in the UK. Feasibility study by Siemens Energy is ongoing. Pass.

195) Engage XR Holdings (Ticker: EXR)

5£m training, education and collaboration platform enabling virtual classrooms through virtual reality for example. Operates highly unprofitable on declining revenue, highlights economic slowdown as the reason. I’d argue its some post-covid normalization for products like this. CEO is the founder, pass.

196) EnSilica (Ticker: ENSI)

41£m fabless designer and supplier of ASICs (Application Specific Integrated Circuits). Recently secured large contracts, but highlights delay in other projects similarly. Expects 20£m revenues for 2025 with a max. 0,5£m EBITDA, guided for 5£m. Growth expected in 2026 with up to 35£m revenues in 2026 with most revenue already secured. Operates unprofitable and FCF negative, but it appears management is focused on scaling the business. Co-Founder from 2001 is the CEO and owns 20% of shares. Has not operated profitable in recent years. Pass.

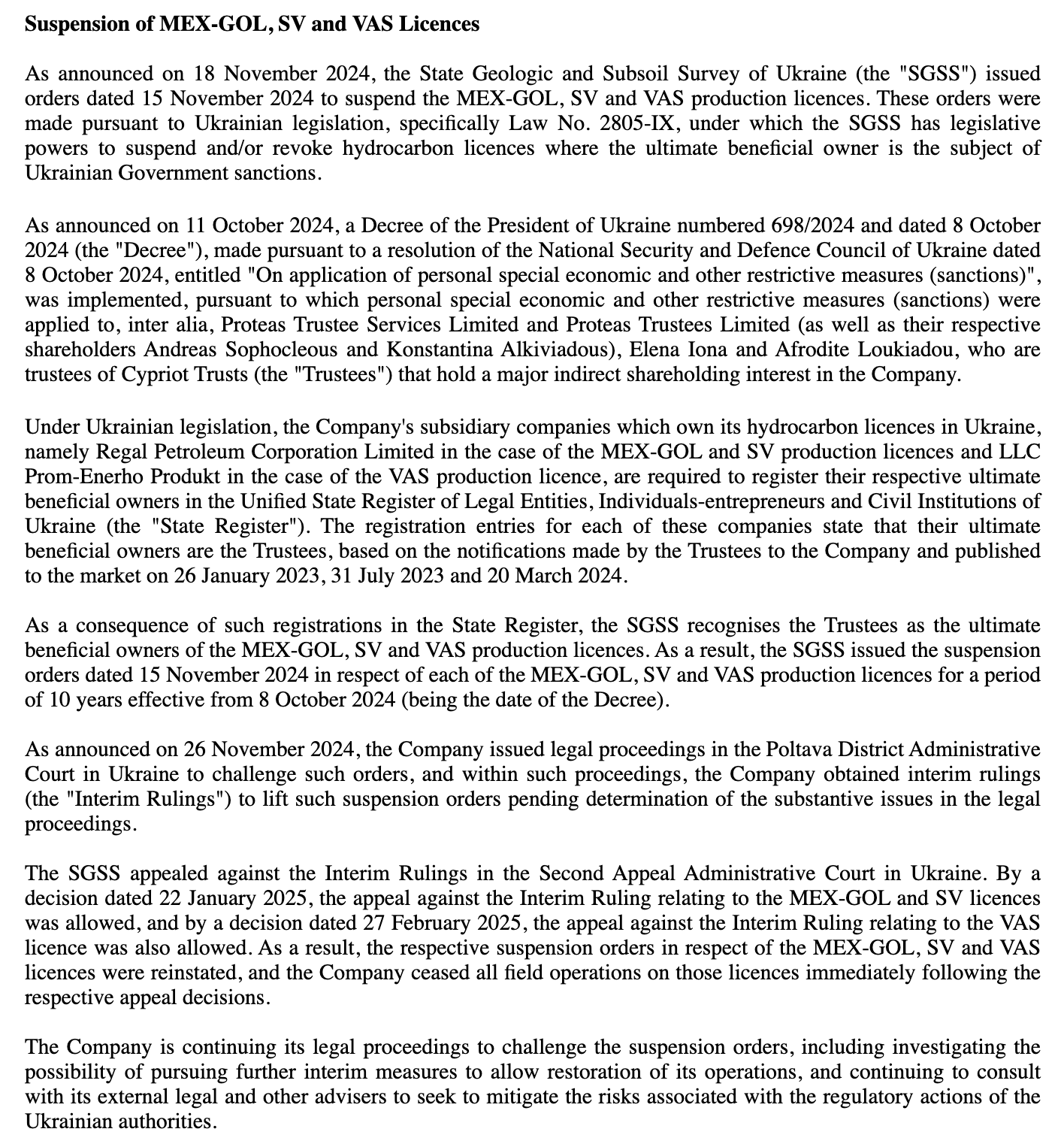

197) Enwell Energy (Ticker: ENW)

48£m O&G exploration and development company from Ukraine. Its production licenses for its fields are currently suspended.

Holds 100$m in cash and is in the exploration process of another gas field. Operated highly profitable in 2024 and 2023. If operations resume and assuming similar profits to prior years, it’s trading on 2x P/E excluding the big cash pile. I can’t tell what’s the detailed plan here, but this one may be worth a look for special situation and O&G investors. Pass.

198) EPE Special Opportunities (Ticker: ESO)

42£m company targeting growth capital and buy-out opportunities, special situations and distressed transactions. Reduced share count by 20% since 2020. States NAV is twice the current share price, NAV grew 9% per share over the last decade. As of 31st Jan 2025, the portfolio consists of 6 companies with a focus on consumer brands: LED lighting, tea, coffee and hot chocolate, homeware, furniture, dog snacks and an online pharmacy.

Seems to be managed by the board without an usual C-suite, all got typical finance background. No notable insider ownership. Likely worth a look into their track record to judge how interesting this one really is considering discount to NAV and buybacks, but special situation PE is simply not my cup of tea, I prefer the long-term ownership found in serial acquirers. Pass.

199) Epwin Group (Ticker: EPWN)

124£m manufacturer of energy efficient and low maintenance building products. Received a cash offer of 120p per share yesterday, therefore the share priced jumped to roughly that price. Directors own only 0,6% of shares, but consider the offer to be fair and recommend shareholders to vote in favor of the deal. Pass.

200) EQTEC (Ticker: EQT)

3£m licensor and innovator of syngas technology for clean conversion of the world’s waste into sustainable energy and biofuels. Multiple projects ongoing. It appears no plant is fully operational, therefore is highly unprofitable. Pass.

Wrap-up

200/669 companies covered so far.

Watchlist: 30/200.

Pass: 170/200.

No-Revenue counter: 44/200.

Feel free to provide opinions and sources on any of the stocks. Cheers.

You're doing good work going through this dross. Hopefully, you'll find a diamond or two in there. Have you considered having a regularly updated article that highlighhts just those that make it to the watch list? You could link to it at the bottom of each A-Z

Thanks, great work as always. One of the worst sets of the whole collection in my opinion…