as the name suggests, this is the start of my A-Z journey. Going A-Z means looking at every stock listed on the exchange, in my case, the alternative investment market (AIM) in London. There are a lot of people who did this on different exchanges, but I want to mention @Memyselfandi007who did a series like this on belgian stocks, as I’ll structure my A-Z in a similar way:

There are over 650 stocks, market caps up to 3£b. I want to put every stock into one of the following categories for me:

Pass: Stocks that I consider to be uninteresting/uninvestable for me e.g. due to high debt load, consistent unprofitability, bumpy financials, unfavorable industry, ‘too hard pile’, …

Watchlist: Stocks that generally seem interesting due to stable growth, solid margins, understandable business model, seemingly smart capital allocation, strategic reviews, C-suite changes, … but where I don’t see a reason to ‘rush’ into researching it deeper because of an unexciting valuation or other reasons that seem to give me some time until I ‘have to’ look at it.

Buy: Stocks where the setup seems so promising, that I am immediately thinking about digging deeper and may buy a starter position. Stocks here combine reasons for ‘Watchlist’ with a low valuation and/or short-term catalysts.

What I consider the be a buy or pass is likely different from others opinions. That’s why I’ll mention all the stocks that are a pass for me, as it may trigger someones interest in the stock or someone who did the work shares their information and corrects my view. So I hope to generate some ideas for myself and others with this series.

I try to post an article weekly and cover between 15 to 30 stocks with each, depending on how much I have to say about the stocks I find. I also look for write-ups of other investors on watchlist companies and provide links in case.

Let’s start with number 1 to 18!

1) 1spatial (Ticker: SPA)

A 55,65£m company that considers itself to be the ‘‘Market-leading patented software platform for Location Master Data Management’’. Providing software and services that help organizations ensure their location data is accurate. I honestly have a hard time understanding what they do in detail, reading about case studies it seems like a data management platform.

No/low insider ownership, but CEO is in her role since 2017. They do 3/4 of their revenue in Europe, planing to expand their US business with a traffic management software. In transition to a SaaS business, >60% is recurring revenue already and keeps growing. As usual in software businesses we see gross margins consistently >50%. Nevertheless EBIT Margin is <5% due to high S,G&A costs. According to their recent trading update from March they expect to see further growth in FY26. FY25 growth was <5%. P/E >35.

Pass: Transition to SaaS is interesting but hard to understand product for me, low margin, slow growth despite high S,G&A costs, priced for higher growth. Reading about it makes me think if PE couldn’t buy it to double margins.

2) 450 (Ticker: 450)

14£m no revenue investment vehicle that wants to become ‘market leader in the tradional and digital creave industries, capitalising on the ongoing transformaon of the content, media and technology sectors as well as considering opportunies in e-commerce and retail.’ Pass.

3) 4BASEBIO (Ticker: 4BB)

180£m unprofitable biotech company valued at >100x/sales. They recently received a certification to manufacture in their UK facility, appointed a Chief Commercial Officer and the Royal Bank of Canada initiated sell-side coverage.

Easy pass for me as I have no clue about biotech, but it seems like that something is happening.

4) 4Global (Ticker: 4GBL)

7£m software/data company focused on major sporting events and promotion and measurement of physical activity.

Business description: https://investors.4global.com/about-4global/

Doing about 5£m in revenue, 60% in Europe. Currently shifting their activity in the middle east to the USA. Also shifting away from a project-based low margin to a high margin and recurring revenue model. Profits were bumpy in the past. CEO owns >50% of shares and is an advisor to the UK government. IPO’d during tech hype 2021 and lost 75% of its value.

Watchlist: It’s close to a pass due to bumpy profits, too high ownership of one single person and I am not sure if the niche they try to place themselves in even exists. But in 2026 the FIFA World Cup will take place in North America and maybe they gain some traction as they shift their activity.

5) 80 Mile (Ticker: 80M)

Zero revenue mining company with projects in Italy, Finland and Greenland. Easy pass: no revenue = no watchlist.

6) 88 Energy (Ticker: 88E)

Zero revenue oil & gas exploration company with projects in the USA and Namibia. Having no revenue but being listed on 3 stock exchanges, always a good sign for a quality company 🚩. Easy pass: no revenue = no watchlist.

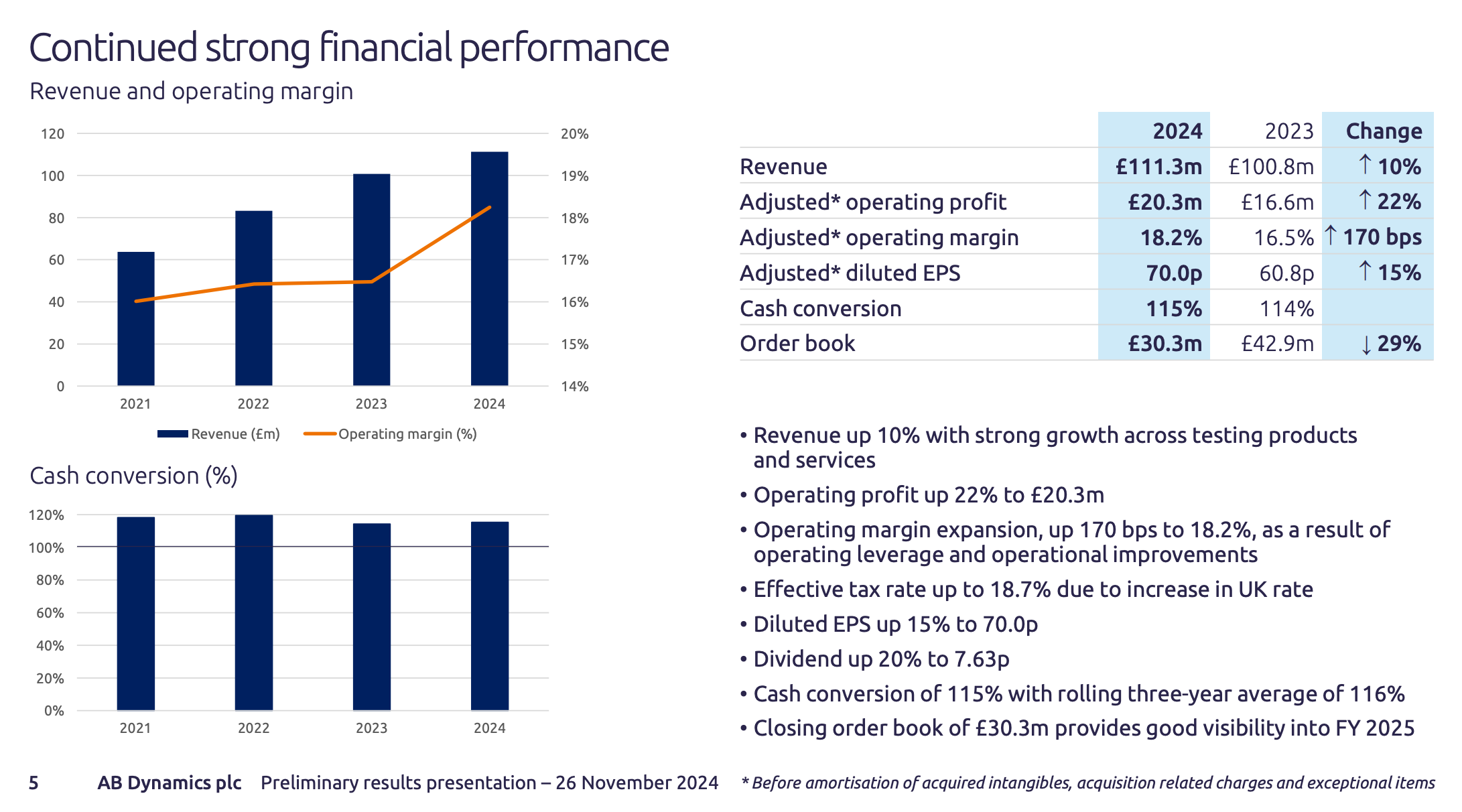

7) AB Dynamics (Ticker: ABDP)

A 360£m market cap company providing automotive test and verification solutions like test-targets/dummies, driverless test systems and sensors to monitor impacts. First impression is those are critical tools for car manufacturers, especially for R&D.

The Company is consistently growing, doubled its revenue since 2020 while increasing margins and maintaining a net cash position. Small C-suite: CEO & CFO. Annual bonuses are paid based on EBIT, EBIT margin, order intake, cash conversion, TSR and EPS.

No long-term debt on the balance sheet. 40% of long-term assets is goodwill. In H1 2025 they grew 11% and are confident to keep up the momentum for the year.

Full Year Results 2024 Presentation

In November 2024 medium-term targets were released guiding for 10% average organic growth while increasing profitability further. On an adj. EPS basis its trading at around 20x forward P/E.

Watchlist: Interesting niche, consistently growing business. Need to dig deeper into capital allocation and how cyclical the demand is here. Probably fair valued.

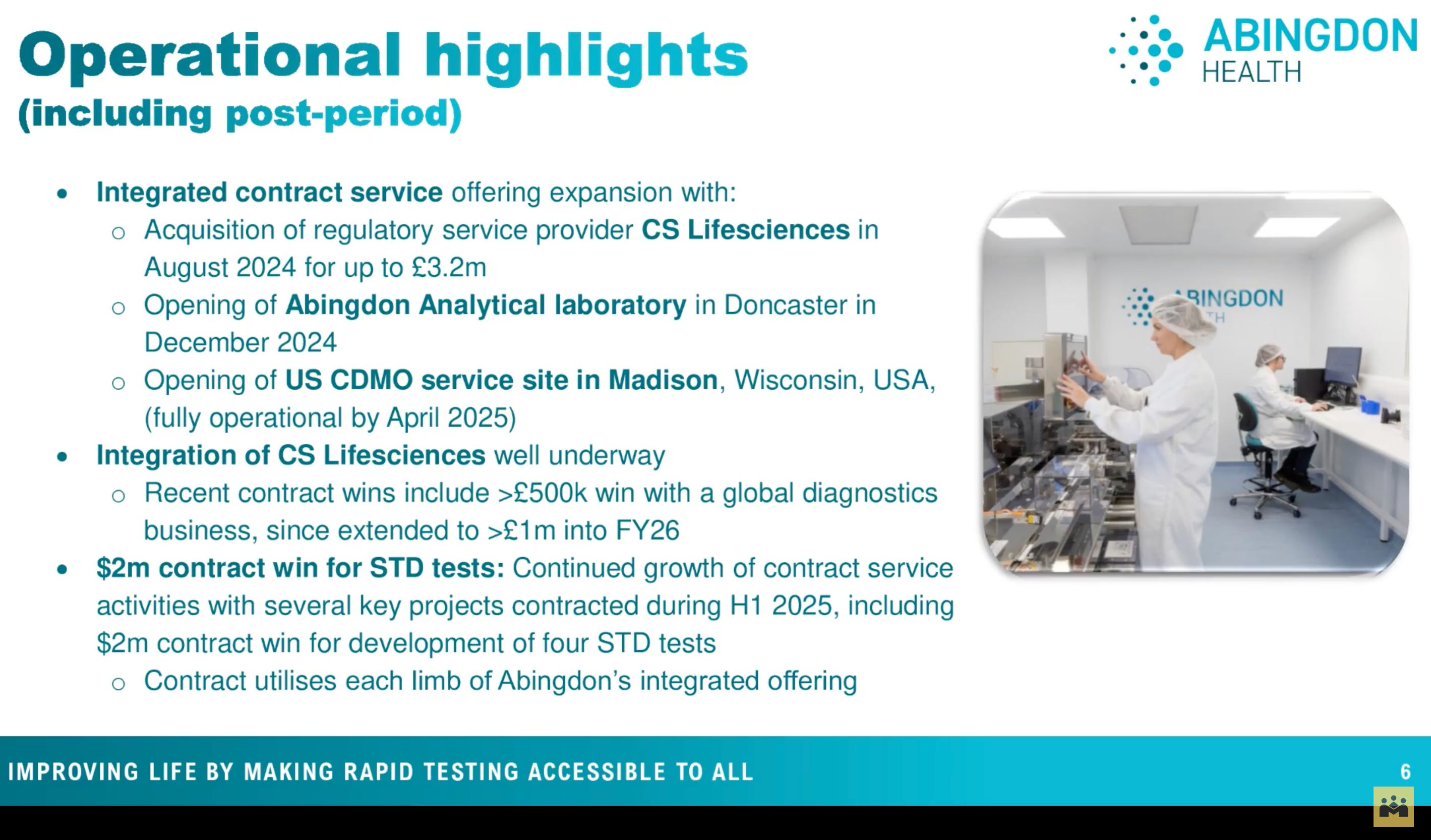

Abingdon is a contract developer and manufacturer of rapid tests and offers its own self-tests to consumers. The Co-Founder is still involved. He was CEO until March 2025 and now leads the operations in the USA. As with 4Basebio, it seems that things are moving forward:

H2 2024 Presentation

Currently unprofitable, they aim to be cash flow positive in calender year 2026. Market cap of 11£m, revenues of 3£m.

Pass: Even though rapid tests as a product are way easier to understand than other biotech business models I usually avoid unprofitable pharma stocks. Even the profitable ones are mostly in the ‘too hard pile’ for me.

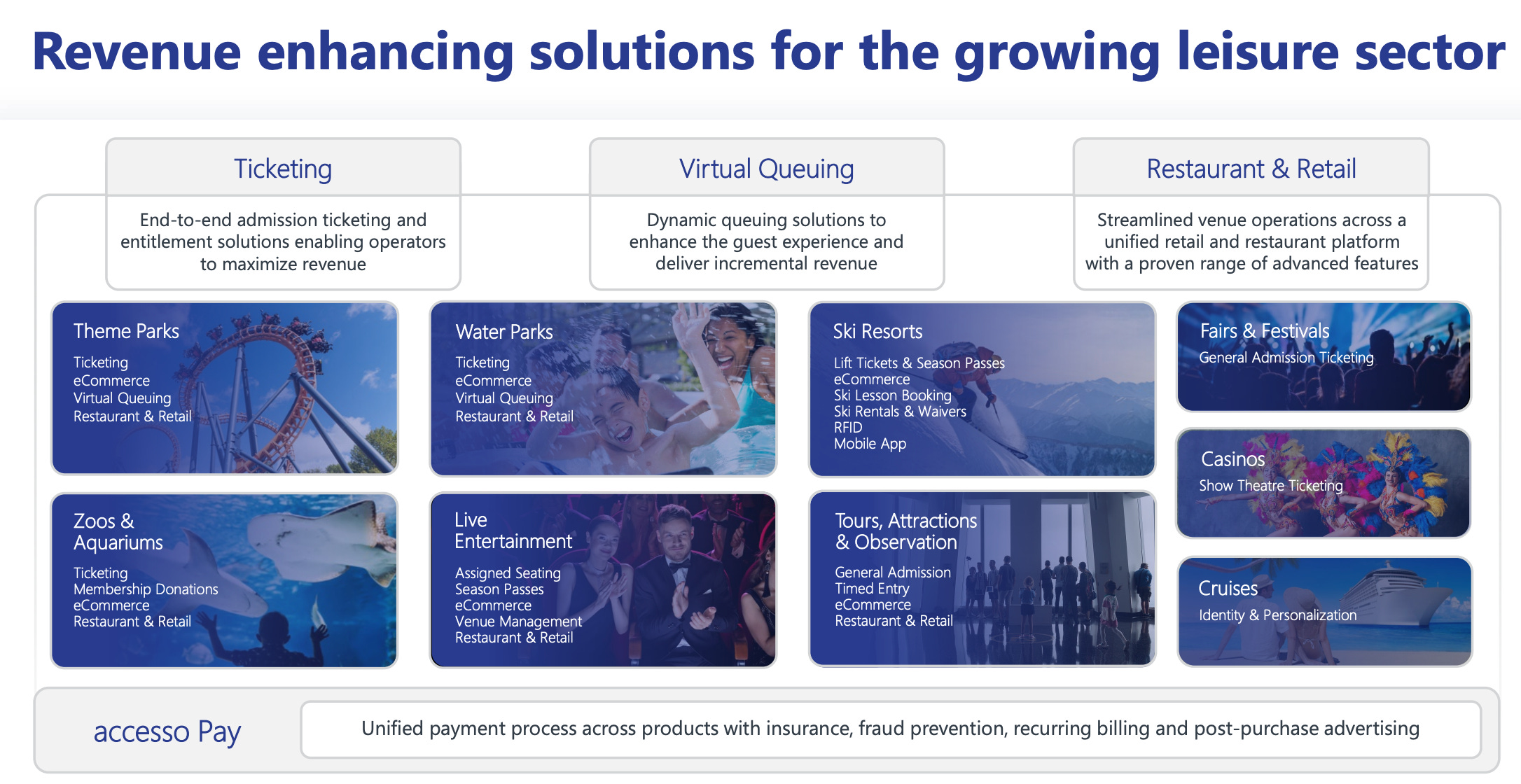

9) Accesso Technology (Ticker: ACSO)

180£m company providing solutions for the leisure sector, mostly UK and US. Most revenue is generated from ticketing and eCommerce. 78% gross margin, 7,5% EBIT margin.

Full Year 2024 Presentation

For 2025 they do not expect to achieve more than 5% growth. Valued at 9x fwd. EV/EBIT. Net cash on the balance sheet. Low insider ownership. SBC about 2% of revenue.

The Board maintains its consistent view that the payment of a dividend is unlikely in the short to medium term with surplus cash more efficiently invested in share repurchases, strategic product development or, where the opportunities arise, value accretive acquisitions.

Board just approved a 8£m buyback program (roughly 5% of shares) after completing the old one and hired new COO. CEO worked for Disneys Disneyland Resort in the past and in other ticketing related jobs.

Watchlist: Interesting niche where they should be able to grow by adding more venues, CEO seems to be an expert in his field. Board likes buybacks. Valuation is not demanding, but also not exciting considering limited growth opportunities.

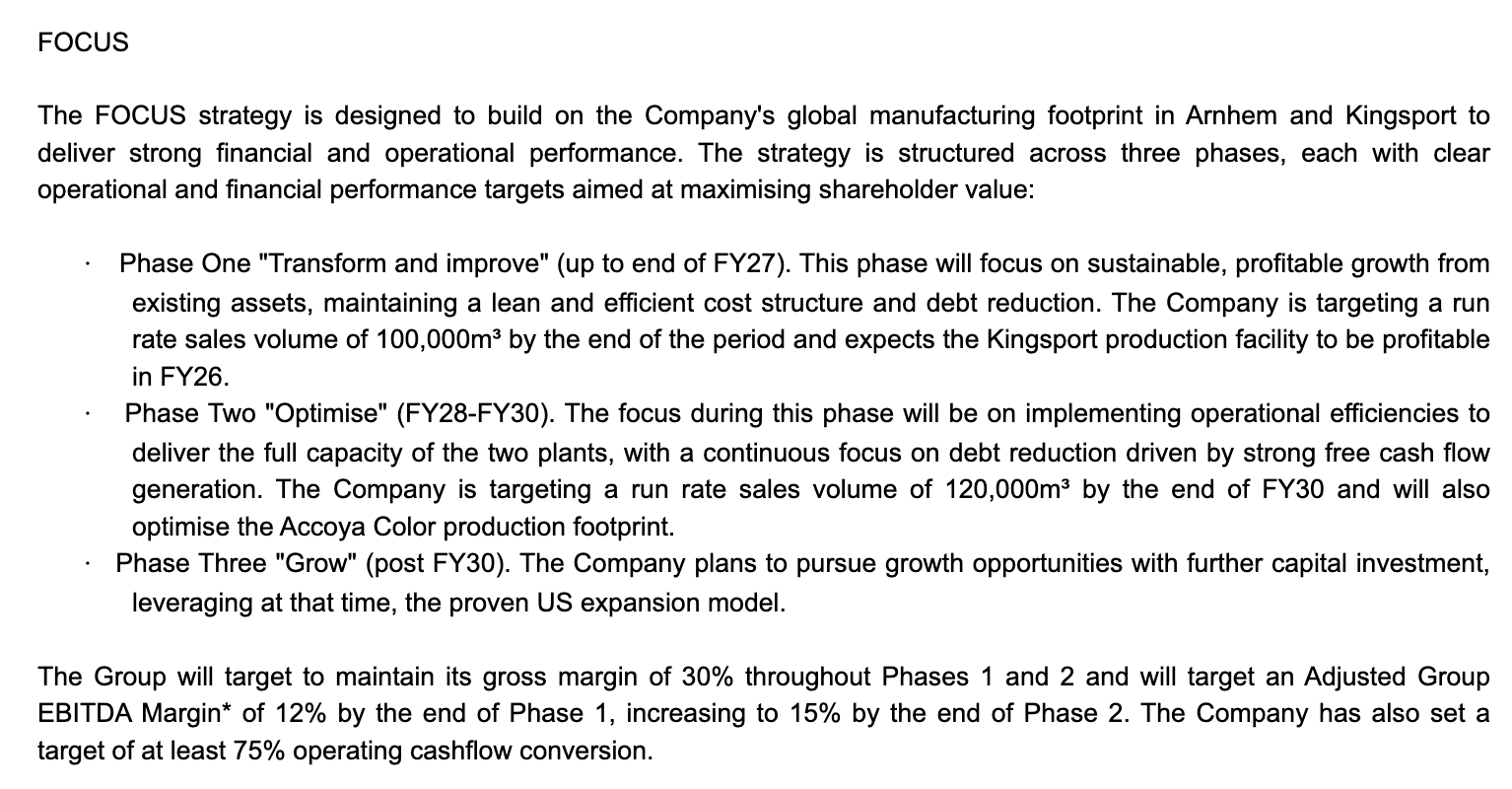

10) Accsys Technologies (Ticker: AXS)

Accsys, the world’s leading supplier of premium, high performance and sustainable wood building materials. We combine chemistry, technology and ingenuity to make high performance wood products that are extremely durable and stable, opening new opportunities for the built environment.

Recent strategy update

The recent strategy update targets 12% adj. EBITDA margins. In H1 FY25 we saw 5,5%. Shares outstanding increased by 20% in the last 3 years. CEO and CFO are with the company for < 2 years.

Assuming 140£m in revenue and 12% adj. EBITDA margin leads to EV/adj. EBITDA of 8,7. Debt load could become a problem in tough times. Likely exposed to a cyclical industry and price fluctuations. Pass.

11) Active Energy (Ticker: AEG)

0,35£m biomass energy company. Just announced a new patent. No revenue. Pass.

12) ActiveOps (Ticker: AOM)

60£m provider of decision intelligence software to assist data-based decison-making. 90% of revenue recurring, steady 10% grower. >100% net revenue retention rate.

Co-Founder is CEO and owns 14% of shares. Debt free. But valued at 30x fwd EV/EBIT or 40x fwd. P/E and customer concentration (2 customers account for 24% of revenue, top 10 customers for 58%) makes it a pass.

Feel free to subscribe to follow my A-Z journey.

13) ACUITY RM GROUP (Ticker: ACRM)

Unprofitable 2£m market cap company providing risk management software related to cybersecurity risks. Grew 50% in 2024. Such a small unprofitable company in a field I have no interest in and no understand for is a pass.

14) ADM Energy (Ticker: ADME)

1,4£m O&G company. Can’t even find recent reports. Pass.

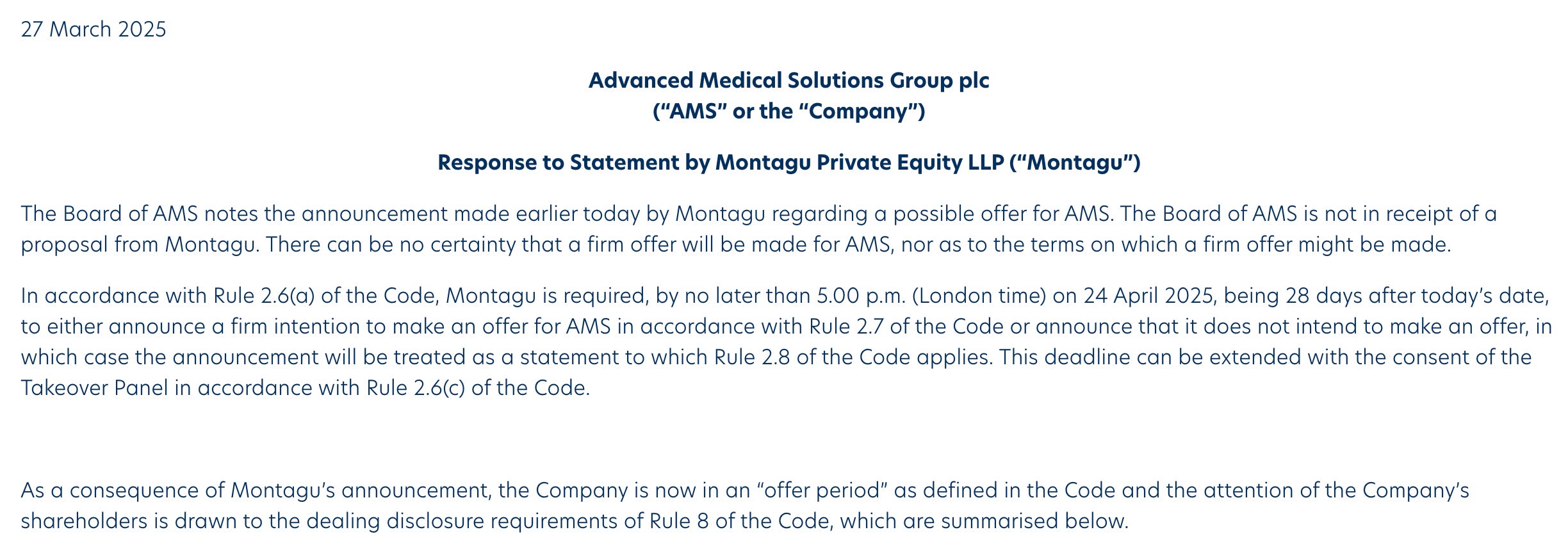

15) Advanced Medical Solutions (Ticker: AMS)

With 410£m market cap the largest company so far, which provides tissue-healing products like bone substitutes and wound-healing or infection control technology. There are rumors of a public takeover offer from Montagu, a private equity company:

Montagu said: ‘‘There can be no certainty that any firm offer will be made and a further announcement will be made as and when appropriate. Any offer, if made, is likely to be solely in cash, although Montagu reserves the right to vary the form of consideration and/or introduce other forms of consideration.’’

RNS Statement by AMS

That was 3 weeks ago. So far I only found a public opening position disclosure by a party to an offer stating that Montagu owns 0 shares in AMS as of 9th April. Montagu has until 24th of April to make an offer.

The stock price jumped 20% as the rumors came up, but crashed back to old levels quickly.

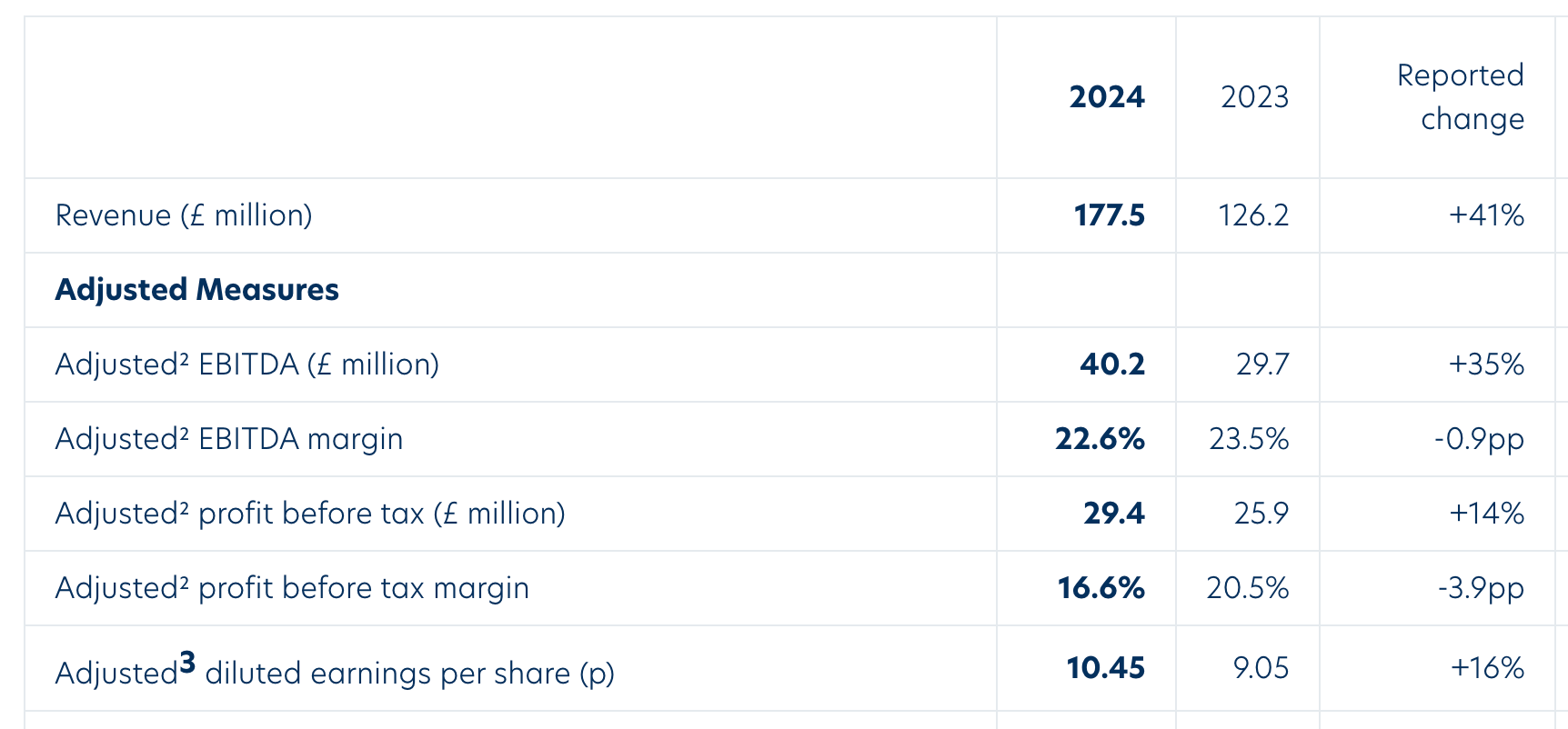

Full Year 2024 Report

Growth in 2024 was driven by a big acquisition for 113£m (1,5x revenue). The adj. numbers above are mainly adjusted for the M&A expenses. As they took some debt to finance the acquisition, EV/adj. PBT sits at 16, but roughly 50% of M&A impacts are missing as the deal was closed mid year. According to Koyfin the fwd. P/E is 15. Paying a 1,5% dividend.

The CEO is with the company since 2005 and in his role since 2011. The Chair of the board was non-executive director in a healthcare company that has been acquired for 2,8£b in 2021. The two other directors also got M&A experience. There seems to be no insider who owns many shares.

Watchlist: No matter if there will be an offer or not this seems to be the most interesting so far. Experienced management team, undemanding valuation in a rather non-cyclical industry. Definitely more work needed on the big acquisition they made. Growth before covid was 10% on average.

16) AdvancedAdvT (Ticker: ADVT)

AdvT is offering different software products: financial management, healthcare intelligence compliance and benchmarking, resource planning and talent management, workforce management and a software for intelligent document processing.

Board expects adj. EBITDA (only adjusted for M&A and listing expenses as they ipo’d in 2024) to be above 8,4£m for FY25. With a market cap of 200£m that’s at least an elevated valuation. But 80% of revenues are recurring and we saw 30% growth recently.

CEO was involved in 3 software exists in leading positions so far and owns 13% of shares, CFO was involved in one of them as well. Other big shareholders are PE companies. As of August 2024 they had 83£m in cash and no debt. Seem to have an M&A focus.

Pass: High growth valued for high growth is not my cup of tea but with that much cash on hand and experienced software and M&A people it may be interesting for software & PE investors.

17) ADVFN (Ticker: AFN)

A 2,5£m company with negative enterprise value. Exciting? Not really. The board currently seeks shareholder approval to cancel AIM trading. There seems to be no ‘take private’-bid, but a ‘matched bargain facility’ which allows for trading through a certain broker. General meeting will be on April 25th.

The company operates finance websites similar to Yahoo Finance. Revenues jumped to nearly 8£m during the 2021 covid bubble, but plunged to 5,5£m in the following year. CEO changed, the new winded down some operations and cut costs. For the 6 month ending December 2024, revenue was 2£m while a 500£k operating loss is eating up the cash pile.

Pass: even if AIM trading is not cancelled the product is uninteresting. Absolutely no moat, no scale with this size. The CEO is there since 3 years and isn’t even close to profitability. There is a lot of AI, state-of-the-art, cutting-edge bla bla in the recent report. No mention of liquidation.

18) Aeorema Communications (Ticker: AEO)

A 4£m company providing corporate communication services, organizing corporate events and consulting. Currently undergoing a cost saving and restructuring program. Chair expects to deliver 0,55£m profit before tax in the current fiscal year. H1 report shows unprofitability but that seems to be due to seasonality of revenues and profits weighted towards H2. Therefore, it’s trading on 7x market cap/pbt.

Quadrupled revenue since 2018, but low predictability of revenues. 800£k cash on the sheet with no long-term debt. Board and CEO own 35% of shares. Paying a 6,5% dividend.

The biggest event for the company seems to be the Cannes Lions International Festival of Creativity, mentioned by the sell-side analyst who also mentions low predictability and does not provide future estimates. According to annual report 2024 the biggest customer accounted for 15% of revenues.

Watchlist: Probably not the easiest industry to operate in, but high insider ownership, low valuation, high dividend and strong historic growth makes it interesting enough to keep an eye on. With 4£m market cap this is highly illiquid of course.

Wrap-up

18/669 companies covered so far. Watchlist: 5/18. Pass: 13/18.

Feel free to provide opinions on any of the stocks and feedback on the structure of this article. Cheers. Below you find the other articles of this series.

Thanks for reading! Feel free to subscribe to follow my A-Z journey.

great read AMS seems intresting, will have a look as wel.

Thanks so much! Looking forward to the next 585 :)